Key Points

- Immediate Tax Recalibration: Updating W-4s instantly prevents the tax refund trap, keeping vital liquidity in your portfolio rather than providing interest-free government loans.

- Strategic Asset Conversion: Leveraging the new 529-to-Roth IRA rollover provision transforms excess education savings into a powerful, tax-free retirement engine for your dependents.

- Automated Wealth Scaling: Implementing successor savings triggers captures freed-up cash flow from child-rearing milestones, preventing lifestyle creep and accelerating multi-generational growth.

Table of Contents

- The Invisible Cost of a Growing Household

- Decoding the Numbers Behind Expanding Families

- Escaping the Interest-Free Government Loan

- Building a Fortress Around Your Lineage

- Repurposing Education Funds for Retirement

- Rewiring Your Financial Brain for Multi-Generational Growth

- The Dawn of the Automated Family Office

- A New Era of Financial Agility

The Invisible Cost of a Growing Household

Picture bringing a new child home from the hospital, exhausted but overjoyed. Unknowingly, you might trigger a cascade of financial leaks across your portfolio. While you adjust to sleepless nights, a silent information gap begins draining your resources.

Families routinely lose an average of $4,500 in the first year of a dependent change. This happens simply due to delayed tax withholding updates and missed credit opportunities. It is a structural failure in how we manage sudden life transitions.

To plug these leaks, ambitious families must embrace Lifecycle-Dependent Wealth Realignment. This strategy moves beyond basic budgeting to transform your growing household into an optimized financial ecosystem.

Treating a change in dependents as a catalyst for strategic adjustments turns potential friction into a compounding engine. It aligns your daily cash flow with your multi-generational legacy from day one.

Decoding the Numbers Behind Expanding Families

Market Intelligence & Data

Lifetime Child-Rearing Cost

The estimated total cost to raise a child born in 2026 to age 17, adjusted for projected inflation, according to the 2026 Brookings Institution economic update.

The Insurance Coverage Gap

The percentage of households with new dependents who report being ‘significantly under-insured’ for death or disability, per the 2025 LIMRA Insurance Barometer Study.

Education Inflation Surge

The observed increase in private university tuition costs over the trailing three-year period ending in 2026, based on the College Board’s 2026 Trends in College Pricing.

529-to-Roth Conversion Cap

The maximum lifetime amount allowed for tax-free rollover from a 529 plan to a Roth IRA as fully implemented in the 2026 tax year under SECURE Act 2.0.

The staggering $351,000 price tag to raise a child born in 2026 is a wake-up call for proactive wealth management. This figure represents far more than just groceries and clothing. It is a massive capital allocation that requires strategic cash flow planning.

Without a deliberate wealth realignment, this expense can easily derail your primary retirement timeline. Equally concerning is the 44% insurance coverage gap among households with new dependents.

Failing to update risk management profiles leaves your growing lineage dangerously exposed to sudden income loss. Closing this gap ensures your wealth-building engine runs uninterrupted during catastrophic life events.

As private university tuition costs surge by 18%, traditional savings methods rapidly lose purchasing power. Families must deploy advanced asset location strategies to maximize tax-advantaged growth.

Thankfully, the new Student Aid Index rules offer a powerful loophole. Because grandparent-owned 529 plans are no longer considered student income, families can shield generational wealth while securing vital financial aid.

Finally, the $35,000 conversion cap represents a monumental shift for over-funded education accounts. Parents previously feared the 10% penalty on non-qualified distributions if a child chose a less expensive college route.

Now, the 529-to-Roth IRA rollover provision transforms excess education savings into a massive retirement head start. It turns a potential tax penalty into a multi-generational compounding machine.

Escaping the Interest-Free Government Loan

One of the most common blunders new parents make is falling into the tax refund trap. Failing to execute an immediate W-4 recalibration causes families to over-withhold their hard-earned money.

This essentially provides the government with an interest-free loan. Meanwhile, the household might simultaneously be carrying high-interest consumer debt.

Proper Lifecycle-Dependent Wealth Realignment requires instantly adjusting these withholdings to retain maximum liquidity. Keeping that capital in your own ecosystem lets you deploy it into high-yield investments or pay down toxic debt.

Furthermore, leveraging the 2026 Child and Dependent Care Credit directly boosts your investable cash flow. Capturing up to $3,000 in expenses for one dependent ensures your child-rearing costs are heavily subsidized by tax efficiency.

Building a Fortress Around Your Lineage

Adding a dependent instantly magnifies your financial responsibilities. This necessitates a robust shield around your growing assets.

A critical strategy here is term laddering, which involves stacking multiple life insurance policies. This precisely covers the 18 to 22-year dependency window, ensuring maximum coverage when your family is most vulnerable.

Beyond insurance, estate settlement can turn into a severe liquidity crunch. This happens if minor children are named as direct beneficiaries without proper trust structures.

Courts will often freeze assets during these transitions. This leaves surviving caretakers scrambling to pay daily expenses while legal fees mount.

Drafting a springing power of attorney and establishing revocable living trusts guarantees seamless wealth transfer. This legal architecture ensures your capital remains highly accessible for your child’s immediate needs.

Repurposing Education Funds for Retirement

Education planning has historically been a high-stakes guessing game. Parents often faced a dilemma where they might over-fund a 529 plan and risk a 10% penalty on non-qualified distributions.

Alternatively, they might under-fund it and rely on expensive student loans. Fortunately, modern wealth architecture completely eliminates this friction.

Under the latest tax provisions, a $35,000 lifetime limit can be moved from a legacy 529 account directly into a Roth IRA. The only major stipulation is that the account must have been open for 15 years prior to the rollover.

This effectively turns a college savings vehicle into a stealth retirement fund. It allows your child to begin their adult life with a massive, tax-free compounding engine already firing on all cylinders.

Rewiring Your Financial Brain for Multi-Generational Growth

Expanding your family triggers a profound wealth identity shift. You are no longer just accumulating assets for your own retirement.

Instead, you are laying the foundation for a multi-generational legacy. However, this psychological shift is often derailed by lifestyle creep.

A larger household size frequently leads to permanent consumption increases rather than scaled investments. To combat this, ambitious wealth builders utilize automated successor savings triggers.

These are pre-set rules that automatically increase your 401k or brokerage contributions. They activate whenever a dependent reaches a specific milestone, such as finishing expensive daycare.

Capturing that newly freed cash flow prevents it from being absorbed into your daily lifestyle. This artificially constrains your budget while rapidly accelerating your net worth.

The Dawn of the Automated Family Office

The sheer manual complexity of tracking tax, insurance, and investment accounts across a growing family is staggering. Currently, parents act as part-time CFOs, juggling dozens of moving financial parts.

Fortunately, the future of wealth management is rapidly shifting toward seamless automation. By 2026, AI-driven family office bots will analyze your real-time spending.

These systems will automatically suggest 529 contribution adjustments based on projected college inflation rates. This eliminates the guesswork and ensures your savings rate perfectly matches future liabilities.

Furthermore, hyper-personalized dependency ledger systems will use blockchain-verified birth records to trigger instant updates. This means your banking, insurance, and IRS profiles will perfectly align the moment your child is born.

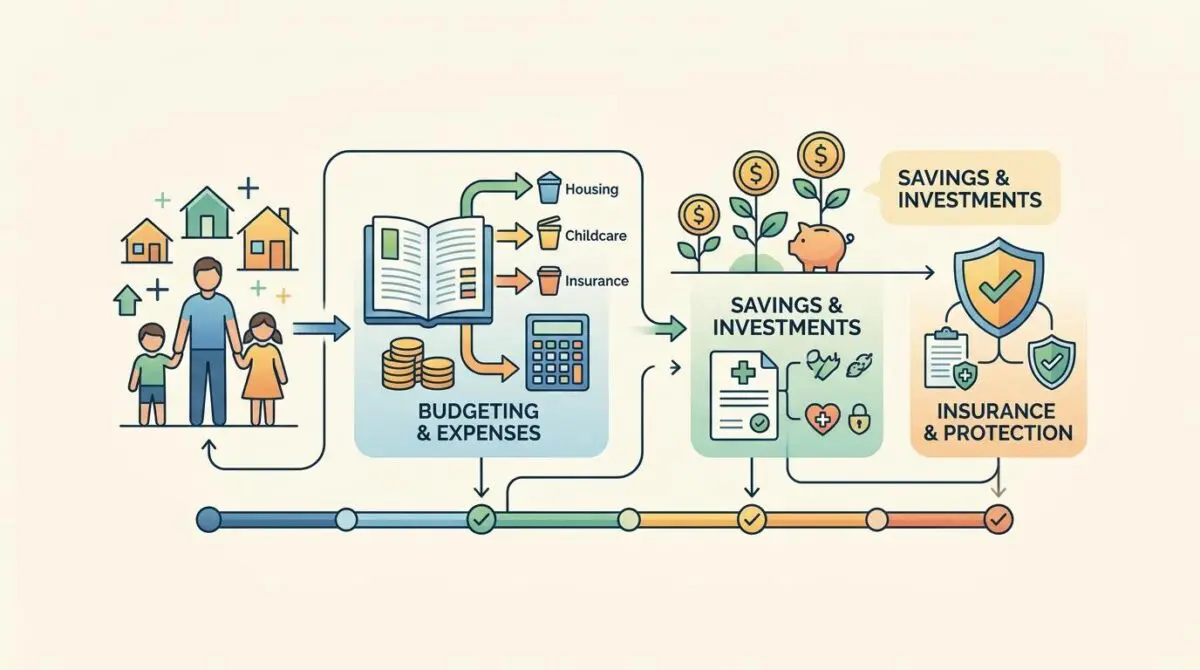

A New Era of Financial Agility

Mastering the transition of a growing family requires more than just a larger emergency fund. It demands a holistic, agile approach to how your money flows, compounds, and protects your lineage.

By actively realigning your wealth at every major life milestone, you transform routine household changes into powerful catalysts. This proactive mindset is the key to lasting financial independence.

Navigating the complexities of wealth building, long-term investments, and financial planning requires a sharp strategy. To scale your financial growth and build a resilient digital architecture for your business, connect with Andres at Andres SEO Expert.

Frequently Asked Questions

What is the financial impact of delayed tax withholding updates after a dependent change?

Families often lose an average of $4,500 in the first year of a dependent change due to delayed tax withholding updates and missed credit opportunities. Executing an immediate W-4 recalibration is essential to retain liquidity and avoid providing the government with an interest-free loan while carrying potential household debt.

How much does it cost to raise a child born in 2026?

According to 2026 economic updates from the Brookings Institution, the estimated total cost to raise a child born in 2026 to age 17 is approximately $351,000, adjusted for projected inflation. This significant capital allocation requires proactive wealth realignment and strategic cash flow planning to avoid derailment of retirement timelines.

What are the rules for rolling over a 529 plan into a Roth IRA under SECURE Act 2.0?

Under the 2026 tax implementation, families can execute a tax-free rollover of up to a lifetime maximum of $35,000 from a 529 plan to a Roth IRA for the beneficiary. Key requirements include the account being open for at least 15 years, which effectively transforms excess education savings into a multi-generational retirement vehicle.

What is life insurance term laddering for families?

Term laddering is a risk management strategy that involves stacking multiple life insurance policies to provide maximum coverage specifically during the 18 to 22-year dependency window. This ensures that a family is protected during their most vulnerable years without overpaying for excessive coverage later in life.

Why should parents establish revocable living trusts instead of naming children as beneficiaries?

Naming minor children as direct beneficiaries can lead to a liquidity crunch because courts often freeze assets until a legal guardian is appointed. Establishing revocable living trusts and springing powers of attorney ensures that wealth transfers seamlessly and remains accessible for immediate needs without bureaucratic interference.

How do automated successor savings triggers combat lifestyle creep?

Successor savings triggers are automated rules that increase investment contributions (such as 401k or brokerage deposits) exactly when a major recurring expense, like daycare, ends. By capturing this freed-up cash flow immediately, families artificially constrain their budget while rapidly accelerating their multi-generational wealth building.