Executive Summary

- Engineering Efficiency: The transition to agentic architectures has enabled a 1:1,000,000 engineer-to-transaction ratio, fundamentally decoupling operational overhead from volume growth.

- Product Evolution: Product management has shifted from front-end UX to the orchestration of Open Finance APIs and Real-World Asset (RWA) tokenization frameworks.

- Sales Unit Economics: The “Rule of 50” mandate has transformed sales roles into strategic consultants focused on high-margin B2B infrastructure and institutional liquidity.

The Great Institutional Pivot

The financial technology landscape has undergone a fundamental structural realignment. As of 2026, the era of speculative venture-led disruption has been superseded by a period of institutional stabilization. Capital allocation now flows toward infrastructure providers that offer systemic resilience rather than mere consumer-facing novelty. This shift has redefined the core roles within a FinTech organization, moving away from the “growth at all costs” mentality toward a rigorous focus on unit economics and capital efficiency. Global tier-1 banks now control a significant portion of neo-banking liquidity through embedded finance subsidiaries, forcing independent firms to operate with unprecedented lean efficiency.

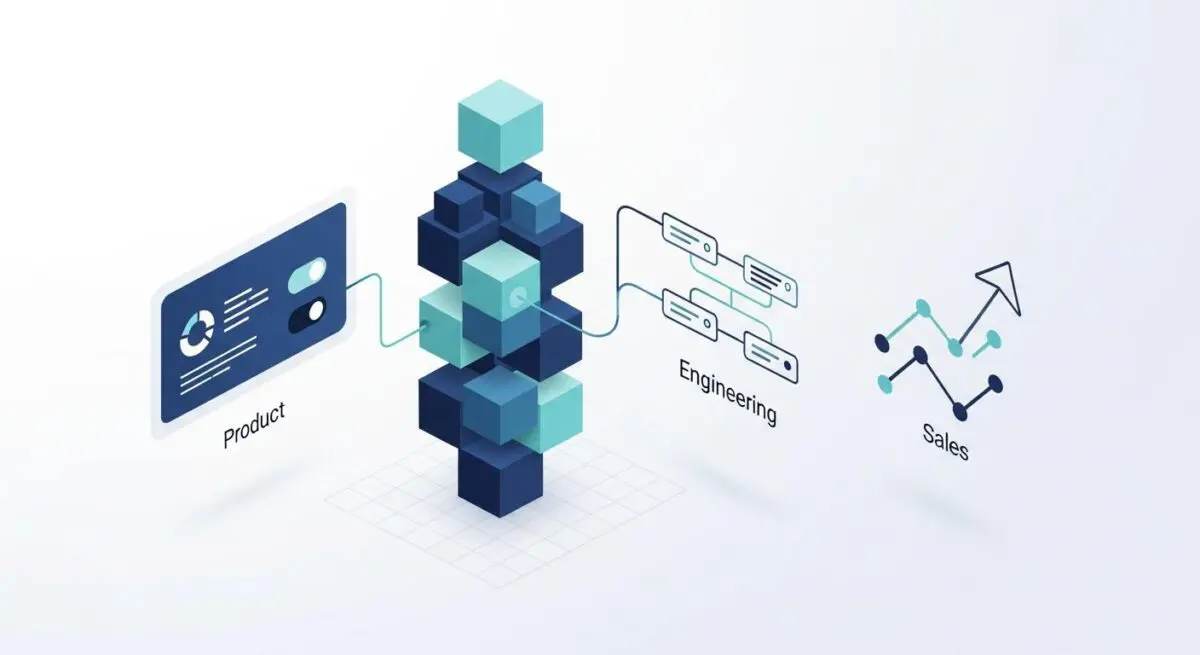

In this high-stakes environment, the traditional silos of Product, Engineering, and Sales have merged into a unified value-delivery engine. The emergence of AI-native firms, often referred to as Lean Scaleups, has demonstrated that a sub-50 headcount can manage assets and volumes previously requiring thousands of employees. This efficiency is not merely a result of better software but a complete reimagining of how financial value is moved, secured, and monetized.

Engineering: From Code Maintenance to Agentic Orchestration

The engineering role in a modern FinTech company has moved beyond the manual construction of payment rails. Today, the focus is on building and maintaining agentic architectures—systems where autonomous agents handle the logic for credit underwriting, fraud detection, and trade execution. This shift has allowed top-tier firms to achieve a transaction-to-scale ratio of one engineer per one million monthly transactions. This represents a massive efficiency gain compared to the infrastructure of just a few years ago.

Modern engineering stacks are now built on “headless” core banking systems that prioritize interoperability and security. With the universal adoption of ISO 20022 standards, engineers are tasked with ensuring that data flows seamlessly across cross-border settlement protocols. Furthermore, the integration of Post-Quantum Cryptography (PQC) has become a non-negotiable standard to protect financial data against emerging decryption threats. The engineer is no longer a builder of features but an architect of a resilient, self-optimizing financial nervous system.

Product Management: Navigating the Open Finance Frontier

Product management has evolved from designing user interfaces to orchestrating complex financial ecosystems. The primary driver of this change is the transition from Open Banking to Open Finance. Under frameworks like PSD3, firms are now mandated to provide access to a broader range of data, including mortgages, savings, and insurance. This has eroded the traditional data moats of incumbent banks, placing a premium on Product Managers who can build superior aggregation layers and personalized financial insights.

A critical component of the modern product roadmap is the tokenization of Real-World Assets (RWA). Product teams are now responsible for bridging the gap between traditional legal ownership and digital ledger efficiency. This involves navigating the “Last Mile” of integration, where digital systems must interface with legacy COBOL-based mainframes. The successful Product Manager in this niche must understand the nuances of T+0 atomic settlement and how to leverage regulated stablecoins to reduce friction in global value exchange.

The modern FinTech infrastructure functions like a high-pressure hydroelectric dam. The Engineering team constructs the turbines and ensures the structural integrity of the walls; the Product team manages the flow and distribution of the water to maximize energy output; and the Sales team ensures that the power generated reaches the high-value industrial grids where it is most needed. If the flow is restricted by legacy friction, the entire system loses its economic potential.

Sales and Growth: The Rule of 50 Mandate

The sales function in FinTech has been recalibrated by the “Rule of 50,” which dictates that a firm’s growth rate plus its profit margin must exceed 50%. This has effectively ended the era of high-burn customer acquisition. Sales professionals are now strategic consultants who focus on B2B infrastructure and institutional partnerships. The goal is no longer just to acquire users but to capture high-margin, recurring revenue through deeply integrated financial services.

Customer acquisition is increasingly automated through AI-driven models that hyper-personalize cross-selling opportunities. This has led to LTV/CAC ratios reaching as high as 6.8x in top-performing firms. Sales teams must now articulate the ROI of “Just-in-Time” (JIT) treasury management and liquidity orchestration, helping CFOs capture additional basis points of yield on idle cash. In this environment, sales is less about persuasion and more about demonstrating technical and economic superiority in a crowded marketplace.

The Regulatory Moat and Operational ROI

Governance is no longer viewed as a cost center but as a strategic asset. The implementation of the EU AI Act and other global mandates has classified financial AI models as high-risk, increasing the cost of compliance. However, firms that invest in real-time compliance architecture—capable of automated SAR filing and instant KYC—see significantly faster time-to-market in new jurisdictions. This “Compliance as a Moat” strategy allows firms to navigate the trust deficit that often slows down the adoption of autonomous financial agents.

The FinTech Lens: Infrastructure & Governance

We at Andres SEO Expert observe that the most successful FinTech entities are those that have successfully decoupled their operational costs from their transaction volumes. The technical shifts toward agentic workflows and atomic settlement are not merely incremental improvements; they are the foundation of a new economic reality. The hidden signal in the market is the move toward verticalized AI stacks that bypass traditional middleware, allowing for a level of agility that legacy institutions cannot match without a total overhaul of their core systems.

Looking forward, the long-term winners will be the firms that prioritize infrastructure interoperability and regulatory transparency. As liquidity continues to fragment across various tokenization platforms, the ability to orchestrate value across these “walled gardens” will define market leadership. Capital allocation will increasingly favor those who can demonstrate a T+0 settlement capability while maintaining the highest standards of cryptographic security. The roadmap to profitability is now paved with technical precision and strategic foresight.

Securing the Future of Financial Value

The evolution of roles within a FinTech company reflects a broader maturation of the industry. From the engineer architecting autonomous logic to the product manager navigating open finance, the focus has shifted to building a sustainable, high-efficiency value layer for the global economy. As the barriers between traditional finance and digital infrastructure continue to dissolve, the strategic alignment of these roles will be the primary determinant of institutional success.

In a landscape defined by rapid technical shifts, strategy is the only sustainable defense. Whether you are architecting for the generative search era or optimizing for operational ROI, the right partnership defines your success. Connect with Andres at Andres SEO Expert to build a future-proof foundation for your enterprise.