Key Points

- Eliminating Financial Latency: Pediatric FinTech Ecosystems bypass traditional banking constraints, allowing Gen Alpha to interact with capital markets long before adulthood.

- Autonomous Wealth Management: AI-governed pocket agents and spatial computing vaults are transforming simple allowance apps into sophisticated, hyper-personalized family offices.

- Programmable Financial Identity: The integration of Decentralized Identity and Pre-Credit Scores prepares minors for institutional lending with a portable financial reputation.

Table of Contents

The Financial Latency Friction

According to the 2026 Global Wealth Transfer Report by Goldman Sachs, the ‘Youth FinTech’ sector has reached a total addressable market of $22.4 billion as Gen Alpha begins managing digital assets at an average age of 8.4 years.

This staggering liquidity event is exposing the critical flaws in legacy banking infrastructure. For decades, the financial industry has suffered from severe financial latency, forcing children to wait until age eighteen to meaningfully interact with capital markets.

Traditional institutions have historically viewed minors as compliance liabilities rather than an emerging asset class. This outdated mindset relies on manual allowance management and abstract digital ledgers that fail to engage digitally native users.

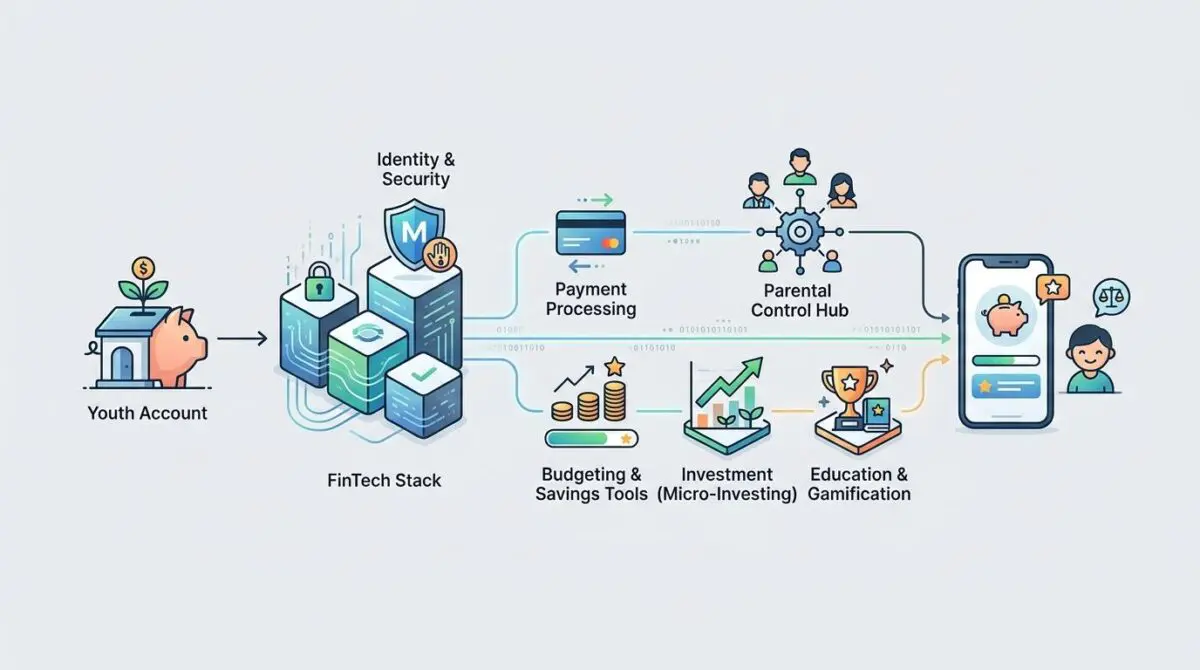

Pediatric FinTech Ecosystems are entirely dismantling this archaic timeline. The ultimate fintech stack for a child is no longer a simple prepaid debit card, but a comprehensive architectural overhaul of generational wealth transfer.

By eliminating these inefficiencies, we are witnessing the birth of a massive liquidity opportunity. This new technological paradigm offers a highly sophisticated, sandboxed environment for early-life asset management that builds robust financial habits from the ground up.

Market Intelligence & Capital Flow

Market Intelligence & Data

Digital Wallet Penetration

According to 2026 Deloitte research, over two-thirds of children in developed economies now use biometrically secured digital wallets as their primary payment method.

VC Inflow for 2025

Data from PitchBook indicates that venture capital investment into ‘Early-Life Wealth-Tech’ hit a record high in the previous fiscal year, focused on AI-driven financial tutors.

AI-Driven Portfolio Alpha

Bloomberg Intelligence reports that youth accounts utilizing ‘Smart-Guard’ AI agents outperformed standard parental-managed accounts by double digits in Q1 2026.

Active Minor Users

Estimates from Statista for mid-2026 show that the top five pediatric fintech apps have a combined user base of 45 million active monthly participants.

Smart Money and Ecosystem Dominance

The data clearly indicates a seismic shift in how institutional capital views early-life financial infrastructure. We are currently observing record venture capital investment into kids’ fintech startups as smart money from tier-one venture firms floods the zone.

Firms like Sequoia and Andreessen Horowitz are aggressively deploying capital into platforms that facilitate programmable inheritance and automated micro-investing. This influx of liquidity is rapidly accelerating the expanding youth fintech market and platforms helping kids secure their financial future at an unprecedented scale.

Market dominance is now fiercely contested between legacy disruptors transitioning to AI-first models and new Wealth-as-a-Service platforms like Z-Alpha and Mint-Gen. These agile startups are building APIs that plug directly into the gaming and social ecosystems where Gen Alpha already spends their time.

Furthermore, Big Tech giants like Apple and Google have quietly integrated minor-mode financial APIs into their hardware ecosystems. This strategic maneuver effectively positions their devices as the primary gateway for Gen Alpha’s initial foray into digital asset management, bypassing traditional banks entirely.

The FinTech Deep Dive

Architecting the Autonomous Family Office

The 2026 pediatric stack has evolved far beyond basic transactional interfaces into what industry leaders call the autonomous family office. Current innovation is heavily driven by AI-governed pocket agents that provide real-time behavioral nudges based on spending patterns.

These hyper-personalized financial literacy modules are transforming how minors perceive wealth accumulation. A 2026 study by the Cambridge Centre for Alternative Finance revealed that 28% of teen-managed portfolios are now overseen by autonomous AI-advisors that rebalance holdings based on real-time social sentiment and gaming-market trends.

Instead of viewing abstract numbers on a 2D screen, children now utilize spatial computing environments to visualize their portfolios. They interact with 3D gamified vaults, making the abstract concepts of compound interest and asset diversification highly tangible and engaging.

This immersive, visually rich approach to financial education is exactly what is helping top pediatric fintech players like Greenlight driving mass user adoption across global markets.

Programmable Inheritance and Smart Contracts

Automation is the foundational cornerstone of this new financial architecture. The massive inefficiency of manual chore tracking has been entirely replaced by automated chore-to-earn cycles powered by smart contracts.

These decentralized protocols enable programmable inheritance, allowing parents to lock funds into conditional smart contracts. Capital is only released automatically when specific educational milestones or behavioral metrics are verifiably met on-chain.

This architecture bridges the gap between traditional banking and Web3 custodial accounts seamlessly. More importantly, this technology addresses the global financial literacy crisis head-on by shifting from theoretical learning to practical execution.

It provides a highly secure, sandboxed environment where children can engage directly with fractional equities and high-yield digital assets. By interacting with real market dynamics early, these platforms are creating a new generation of sophisticated retail investors long before they reach adulthood.

Regulatory Sandboxes and ZKP

Navigating the complex regulatory landscape of minor-owned assets requires flawless cryptographic infrastructure to ensure compliance without sacrificing user experience. The technology layer now relies heavily on Decentralized Identity to provide minors with a portable financial reputation that complies with global KYC standards. Furthermore, these platforms utilize Zero-Knowledge Proofs to ensure absolute data privacy while simultaneously maintaining strict, verifiable parental oversight over all capital deployments.

The Strategic Action Plan

Strategic Trajectory

- Capitalize on the rise of ‘Credit-Building for Minors’ where platform usage generates early financial reputation.

- Utilize ‘Pre-Credit Scores’ to secure preferred interest rates on first-time student and automotive loans from major lenders.

- Drive adoption of ‘Family DAOs’ for collective governance of asset allocation strategies for college funds.

- Deploy ‘Career-Path AI’ agents to suggest high-ROI micro-certification investments based on child behavioral data.

- Strategize for the late 2027 market shift toward pediatric stacks integrated with technical niche earning patterns.

The next eighteen months will definitively separate the visionary platforms from the obsolete legacy systems in the pediatric fintech space. The most critical development will be the rise of credit-building for minors, representing a massive paradigm shift in institutional lending.

Responsible platform usage will soon generate a pre-credit score for younger users based entirely on their digital wallet hygiene. Major financial institutions will leverage these early reputation metrics to offer preferred rates on first-time student or automotive loans, capturing lifetime customers early.

Simultaneously, we anticipate the widespread adoption of Family DAOs across the middle and upper-middle class. These decentralized autonomous organizations will allow extended family members to pool liquidity and collectively vote on asset allocation strategies for a child’s college fund.

Looking toward late 2027, the pediatric stack will deeply integrate career-path AI. These intelligent agents will suggest micro-certification investments based entirely on the child’s spending and earning patterns within technical and creative niches.

Conclusion

The transition from legacy banking latency to real-time, AI-driven wealth management for minors is no longer a theoretical concept. Pediatric FinTech Ecosystems are actively rewriting the rules of generational wealth transfer, turning Gen Alpha into the most financially literate generation in history.

Founders, institutional investors, and banking executives who fail to recognize the power of the autonomous family office will rapidly lose market share to agile, Web3-enabled disruptors. The future belongs to platforms that can safely, securely, and intelligently onboard the youth into the global economy.

Navigating the intersection of financial technology, institutional capital, and market psychology requires a sharp strategy. To future-proof your FinTech architecture and scale with precision, connect with Andres at Andres SEO Expert.

Frequently Asked Questions

What is the current market size of the youth fintech sector?

As of 2026, the youth fintech sector has a total addressable market of $22.4 billion, driven by Gen Alpha members who begin managing digital assets at an average age of 8.4 years.

How does AI improve financial performance for minor-managed accounts?

AI-driven ‘Smart-Guard’ agents help youth portfolios outperform standard parental-managed accounts by roughly 14.2% by utilizing real-time social sentiment and gaming-market trends to rebalance holdings.

What is programmable inheritance in pediatric fintech?

Programmable inheritance utilizes smart contracts to create conditional wealth transfers, where capital is automatically released to a minor only when specific educational milestones or behavioral metrics are verified on-chain.

How can minors build credit reputation before reaching legal adulthood?

Modern pediatric platforms generate ‘pre-credit scores’ based on digital wallet hygiene and platform usage. These early reputation metrics allow major lenders to offer preferred interest rates on student and automotive loans once the user reaches adulthood.

What technologies are used to secure financial data for children?

Pediatric fintech ecosystems utilize a combination of Decentralized Identity for portable financial reputation and Zero-Knowledge Proofs (ZKP) to ensure strict data privacy while maintaining verifiable parental oversight.

What role do Family DAOs play in generational wealth transfer?

Family DAOs are decentralized autonomous organizations that allow families to pool liquidity and use collective governance to vote on asset allocation strategies, such as managing a child’s college fund through a unified smart contract.