Key Points

- Transition from point-in-time appraisals to an AVM Dynamic Recalibration Pipeline for daily, automated LTV tracking across thousands of loans.

- Deploy AI agents to parse unstructured data like MLS descriptions, refining AVM confidence scores by capturing property condition signals.

- Eliminate compliance liabilities by automating daily audit trails and back-testing to meet stringent OCC and FDIC regulatory standards.

Table of Contents

- The Hidden Cost of Stale Property Valuations

- Unpacking the Data Behind Real-Time LTV Tracking

- Overcoming the Daily Grind of Manual Monitoring

- Building the Real-Time Market Data Stream

- Deploying Autonomous Analysts for Unstructured Data

- Automating Regulatory Compliance and Back-Testing

- Measuring the Financial Impact of Automated Pipelines

- Predictive Portfolio Rebalancing and Autonomous Trading

- The Autonomous Future of Mortgage Operations

The Hidden Cost of Stale Property Valuations

Imagine the market shifting drastically overnight while your mortgage portfolio risk exposure remains completely hidden. This happens when teams wait on point-in-time appraisals that take weeks to clear. This static approach to property valuation creates a dangerous lag.

Such delays leave lenders blind to high-equity opportunities and vulnerable during sudden volatility. Manual Loan-to-Value (LTV) monitoring across massive portfolios is no longer just inefficient. It is physically impossible for human teams to manage accurately.

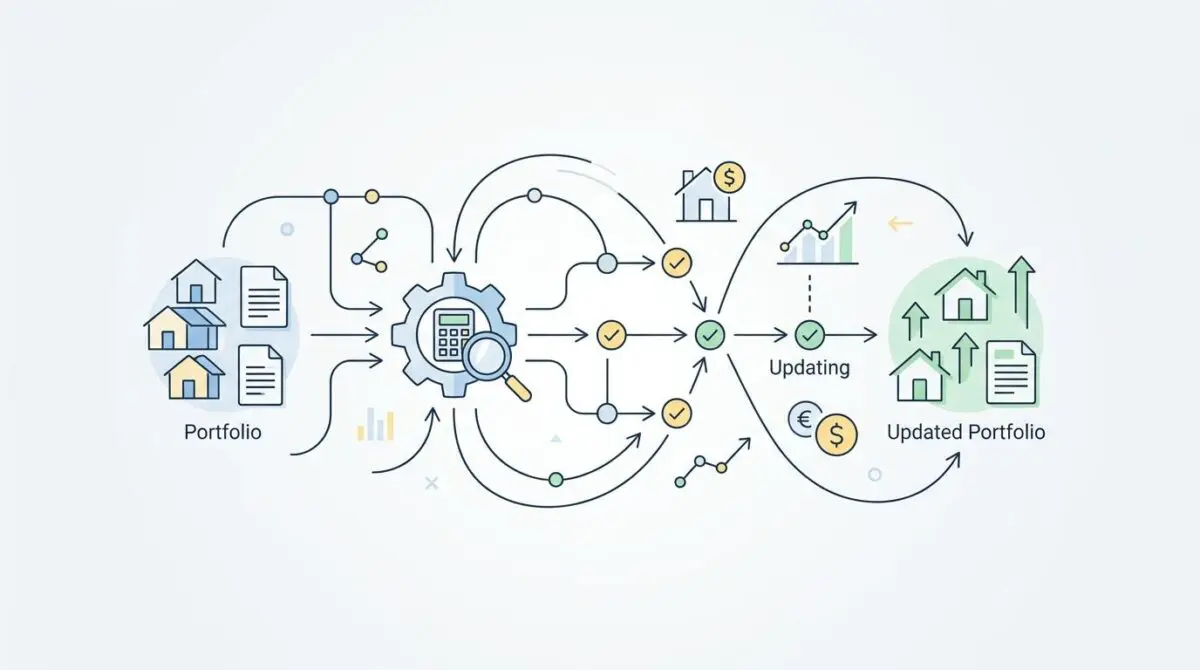

The solution to reclaiming your time and securing your margins lies in deploying an AVM Dynamic Recalibration Pipeline. Replacing outdated manual checks with automated, real-time collateral valuation updates eliminates the guesswork. This pipeline transforms your operations, turning a sluggish compliance burden into a proactive, revenue-protecting asset.

Unpacking the Data Behind Real-Time LTV Tracking

Market Intelligence & Data

AI Decision Speed

According to a May 2026 American Banker report, TD Bank’s new AI agents have reduced mortgage loan application processing time from 15 hours to just a few minutes.

AVM Market Value

A March 2026 report from MarketIntelo confirms the global Automated Valuation Model market reached a valuation of $4.2 billion in 2025, driven by real-time data demand.

Accuracy Improvement

A December 2025 study published in Tandfonline found that incorporating LLM-extracted features into AVMs improved the Mean Absolute Percentage Error (MAPE) by 15.25%.

Cost Savings Per Loan

The 2026 Guide for Lending Operations by Areal AI states that full mortgage automation now saves lenders up to $480 in operational costs per individual loan.

The speed at which financial institutions process data is rapidly redefining industry standards. When AI agents cut mortgage loan application processing time from 15 hours to mere minutes, they eliminate traditional bottlenecks. This rapid turnaround allows lenders to scale operations effortlessly without increasing manual underwriting headcount.

The surge in demand for real-time collateral updates is driving massive capital into valuation technologies. As the global Automated Valuation Model market reaches a valuation of $4.2 billion, institutions are aggressively moving away from static data. This financial commitment underscores the critical need for continuous, live market data feeds.

Accuracy is the bedrock of portfolio risk management, and modern pipelines are pushing mathematical boundaries. Research has shown that integrating advanced data extraction methods significantly improved the Mean Absolute Percentage Error (MAPE) by 15.25%. This leap in precision means fewer margin calls and reduced risk exposure.

Operational efficiency must ultimately translate into tangible financial returns. By automating tedious closing and funding reviews, lenders are seeing operational cost savings average $480 per loan. Furthermore, deploying robust systems that mandates quality control standards for automated valuation models ensures these savings remain intact.

Overcoming the Daily Grind of Manual Monitoring

Lenders have historically relied on point-in-time appraisals that take weeks to finalize. This creates a massive blind spot when managing a dynamic mortgage portfolio. Manual LTV monitoring across tens of thousands of records leads to severe operational lag.

The result is delayed margin calls and entirely missed refinancing windows that cost firms millions in lost opportunity. Today, forward-thinking firms are utilizing advanced tools to bypass this bottleneck. They replace manual tracking with automated daily refreshes of thousands of loan records simultaneously.

Building the Real-Time Market Data Stream

Valuations are fundamentally only as good as the freshest data available. Traditional batches pulled from public records are notoriously sluggish, often lagging months behind actual market shifts. To combat this, next-generation pipelines ingest live data across multiple vectors to trigger immediate recalibrations:

- MLS Listing Updates: Capturing real-time asking price adjustments and days-on-market metrics instantly.

- Off-Market Transactions: Integrating private sales data to maintain a holistic view of neighborhood values.

- Rental Income APIs: Pulling short-term rental data to assess dynamic income-generating potential.

Recent breakthroughs in commercial AVMs integrate real-time Net Operating Income (NOI) estimation and cap rate analytics directly into residential data feeds. This allows lenders to assess mixed-use portfolios through a single API for the very first time. It effectively bridges the gap between commercial and residential risk profiling.

Deploying Autonomous Analysts for Unstructured Data

Traditional AVMs suffer from a critical flaw by remaining entirely blind to actual property conditions. They rely purely on standardized data points like square footage and bedroom counts. This approach misses the nuanced reality of a home’s interior state.

AI agents solve this by acting as autonomous analysts that deeply examine unstructured data around the clock. These agents parse unstructured listing descriptions with incredible speed. They extract housing standard signals and condition keywords directly from the listing text.

This allows the pipeline to dynamically adjust AVM confidence scores based on the actual condition of the property. Such real-world context dramatically increases overall valuation accuracy.

Automating Regulatory Compliance and Back-Testing

Regulatory mandates now require daily, irrefutable evidence of valuation accuracy. Legacy manual spot-checks have transformed from a minor inconvenience into a massive compliance liability. Recent interagency rules strictly mandate that institutions own the risk of their AVMs.

Modern systems must inherently include automated audit trails to survive regulatory scrutiny. They utilize random back-testing protocols to continuously meet stringent OCC and FDIC standards without human intervention. This automated compliance layer ensures that scaling your portfolio does not exponentially scale your legal risk.

Measuring the Financial Impact of Automated Pipelines

Manual post-closing reviews currently face a staggering defect rate based on industry baselines. These errors lead directly to expensive buy-backs and unnecessary capital lock-up. By implementing automated closing disclosure balancing and funding reviews, lenders drastically reduce these costly operational mistakes.

The efficiency gains are nothing short of transformative for the bottom line. Processing times are plummeting from 15 hours to under 30 minutes per file. This frictionless workflow yields operational cost savings averaging $480 per loan, proving that intelligent automation is a pure revenue driver.

Predictive Portfolio Rebalancing and Autonomous Trading

The operational bottleneck is rapidly shifting from simply acquiring data to making decisions fast enough to beat competitors. Autonomous due diligence is transitioning from basic data processing to expert, nuanced interpretation. Systems will utilize LLM-enhanced AVMs to predict portfolio-level rebalancing needs based on hyper-local zoning and sentiment changes.

This shift toward agentic portfolio rebalancing will fundamentally change how assets are managed. Mortgage books will be automatically hedged or sold on the secondary market based on real-time collateral value shifts. The industry is moving definitively from sluggish monthly reviews to autonomous, event-driven trading execution.

The Autonomous Future of Mortgage Operations

The era of static, point-in-time collateral valuation is officially behind us. An AVM Dynamic Recalibration Pipeline is no longer a luxury. It is the foundational architecture required to survive in a high-velocity real estate market.

By embracing live data feeds and autonomous agents, lenders can finally eliminate valuation lag. This approach unlocks hidden equity across their entire portfolio.

Navigating the intersection of technology, workflows, and operational efficiency requires a sharp strategy. To future-proof your business architecture and scale with precision, connect with Andres at Andres SEO Expert.

Frequently Asked Questions

What is an AVM Dynamic Recalibration Pipeline?

An AVM Dynamic Recalibration Pipeline is an automated system that replaces static, manual property appraisals with real-time valuation updates driven by live market data feeds. This allows lenders to continuously monitor Loan-to-Value (LTV) ratios across massive portfolios, eliminating the delay between market shifts and risk assessment.

How does AI improve the accuracy of Automated Valuation Models?

AI improves AVM accuracy by integrating Large Language Model (LLM) features that extract signals from unstructured data, such as property listing descriptions. Research indicates that these advanced data extraction methods can improve the Mean Absolute Percentage Error (MAPE) by up to 15.25%, providing a more precise valuation based on actual property condition.

What are the operational cost savings associated with mortgage automation?

Implementing full mortgage automation and automated valuation pipelines can save lenders approximately $480 in operational costs per loan. These savings result from reducing loan application processing times from 15 hours to minutes and decreasing defect rates in post-closing and funding reviews.

What regulatory standards govern AVM usage in 2026?

Under the 2024 Interagency Final Rule, which took full effect in 2025, financial institutions must maintain strict quality control standards for AVMs. This includes automated audit trails, regular back-testing protocols, and ensuring institutions own the risk of their automated valuations to meet OCC and FDIC compliance requirements.

How do real-time market data feeds improve portfolio management?

Real-time data feeds—including MLS listing updates, rental income APIs, and off-market transaction data—allow for immediate recalibration of collateral value. This enables lenders to perform predictive portfolio rebalancing, identify refinancing opportunities, and hedge mortgage books based on event-driven market shifts.

What is the impact of automation on mortgage processing times?

Modern mortgage automation drastically reduces bottlenecks, with industry leaders cutting loan application processing times from 15 hours to under 30 minutes. This frictionless workflow allows lenders to scale operations without increasing manual underwriting headcount while maintaining higher accuracy in collateral asset valuation.