Key Points

- Parametric insurance replaces subjective claims adjustment with immutable data triggers, enabling straight-through processing (STP) and instant liquidity.

- The integration of Agentic AI and the Internet of Sensors reduces operational claims costs by up to 50% while unlocking dynamic pay-per-use flexibility.

- Institutional capital is shifting toward systemic cyber risk and embedded parametric triggers, targeting a $700 billion global opportunity by 2030.

Table of Contents

The Financial Tech Friction: Decoding the Indemnity Gap

According to GM Insights, the global parametric insurance market is projected to reach $23.85 billion in 2026, growing at a robust 13% CAGR as organizations seek data-driven alternatives to traditional indemnity. This data point signals a monumental shift in how global markets perceive and manage financial volatility. For decades, the insurance industry has been anchored by a fundamentally reactive model.

Traditional indemnity requires a subjective, manual assessment of loss, creating a bottleneck that strangles liquidity when it is needed most. Parametric and On-Demand Insurance shatters this legacy framework entirely. It replaces human judgment with algorithmic certainty, deploying capital based on objective, immutable data.

This is not merely an operational upgrade; it is the financialization of real-world physics and digital telemetry. By treating risk as a programmable variable, smart money is rewiring the fundamental architecture of global protection.

Market Intelligence & Capital Flow

Market Intelligence & Data

InsurTech VC Inflow

Global InsurTech funding is projected to exceed $8.3 billion in 2026 according to research from theinsurtechguide.com.

AI Claims Velocity

Lemonade’s AI-driven platform now closes 40% of property and casualty claims instantly, as reported by Qubit Capital in early 2026.

Weather Parametric Funding

Tracxn data reveals that the weather-specific parametric insurance sector has attracted over $329 million in total venture capital as of Q2 2026.

Regional Market Lead

North America continues to dominate the on-demand insurance landscape with a 37.1% market share according to Fortune Business Insights.

The financial data underscores a massive reallocation of institutional capital toward automated risk mitigation. Venture capital and private equity firms are aggressively targeting the infrastructure layer of the InsurTech ecosystem. They recognize that the future belongs to platforms capable of executing straight-through processing at a global scale.

The broader market trajectory confirms this thesis, as the sector is projected to reach $23.85 billion in 2026, growing at a robust 13% CAGR. This growth is fueled by a convergence of advanced telemetry, decentralized finance principles, and enterprise demand for instant liquidity.

Geographically, the deployment of these advanced models is highly concentrated within mature tech ecosystems. North America continues to dominate the on-demand insurance landscape with a 37.1% market share. This dominance is driven by an established venture network and a regulatory environment increasingly open to algorithmic underwriting.

Institutional Capital and the InsurTech Rebound

The projected $8.3 billion influx into global InsurTech for the 2026 fiscal year is not merely speculative funding. It represents highly calculated, strategic bets by institutional investors seeking shelter from macroeconomic headwinds. These funds are bypassing legacy carriers in favor of agile, API-first platforms.

The thesis driving this capital deployment is rooted in pure unit economics. Traditional insurance models are burdened by massive overhead, legacy IT systems, and human-intensive claims processing. In stark contrast, parametric platforms operate with highly scalable, software-like margins.

Once the initial algorithm is trained and the data oracles are secured, the marginal cost of issuing a new policy approaches zero. This economic reality is why weather-specific parametric funding has surged past $329 million. Investors are recognizing that climate volatility is no longer a tail-risk event; it is a predictable, recurring financial friction.

The FinTech Deep Dive: Immutable Triggers and Agentic AI

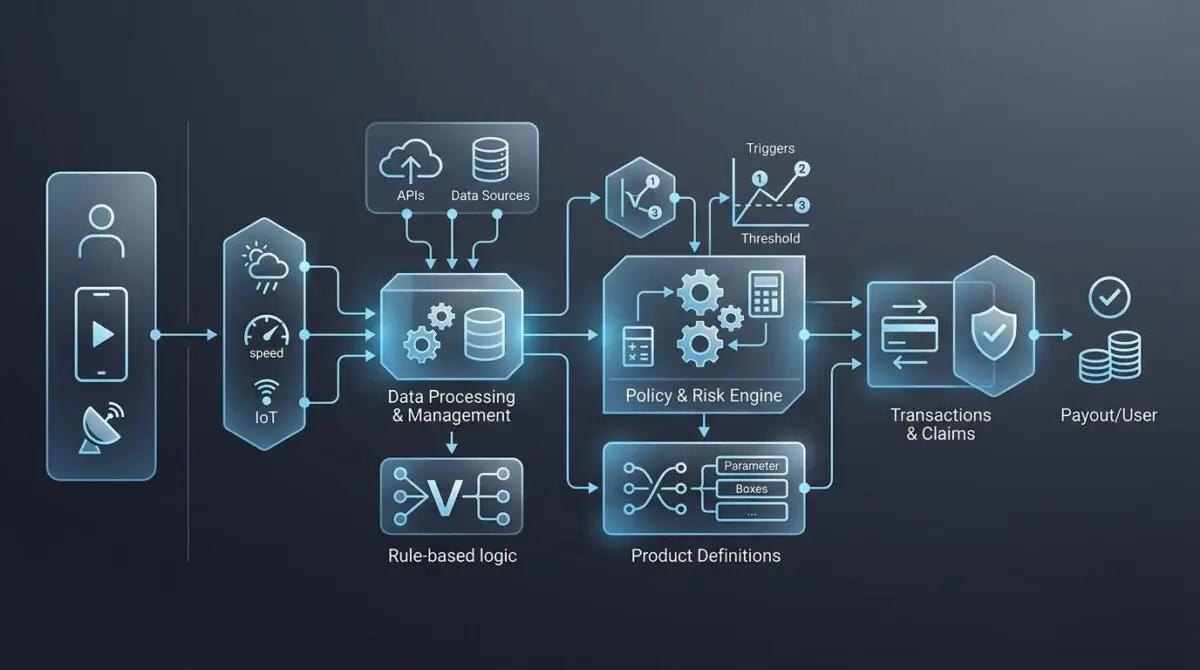

By 2026, parametric and on-demand insurance models have officially transitioned from experimental pilot programs to mission-critical financial infrastructure. The contemporary landscape is defined by the seamless integration of Agentic AI and the Internet of Sensors. This creates a pervasive mesh network capable of real-time, high-fidelity risk assessment.

The Internet of Sensors and Straight-Through Processing

At the core of this technological revolution is the utilization of alternative data streams as immutable triggers. High-resolution satellite imagery from providers like Planet Labs now serves as the undisputed source of truth for smart contracts. These orbital sensors monitor atmospheric pressure, soil moisture, and thermal anomalies with unprecedented precision.

When predefined parameters are breached, these autonomous systems execute straight-through processing with absolute zero human intervention. Payouts are initiated within hours of a verified event, radically transforming the liquidity timeline. Whether the trigger is a seismic shift, a hurricane landfall, or a localized industrial power outage, the capital deployment is instantaneous and exact.

Eliminating the Subjective Proof-of-Loss

This paradigm shift effectively eliminates the indemnity gap that has historically plagued vulnerable supply chains and agricultural sectors. The bloated administrative friction of traditional claims adjusters is entirely bypassed. For smallholder farmers and global logistics managers, the result is critical, near-instant liquidity during severe volatility events.

The operational efficiency achieved through this automation is radically reshaping industry unit economics. Lemonade’s AI-driven platform now closes 40% of property and casualty claims instantly. This velocity of capital is a direct result of behavioral economics AI seamlessly interacting with deterministic payout algorithms.

Data from SAS research reveals that by late 2026, over 35% of global insurers will have deployed autonomous AI agents across at least three core functions, effectively reducing claims processing time by up to 70%. This mid-content insight highlights the rapid institutionalization of autonomous risk management.

By removing the subjective proof-of-loss phase, insurers are successfully slashing operational claims costs by 30% to 50%. Simultaneously, consumers are empowered with dynamic pay-per-use flexibility. This aligns coverage precisely with activity periods, catering perfectly to the transient nature of the gig and sharing economies.

New specialized entrants are aggressively capitalizing on this reduced friction to capture market share. Startups like Gangkhar, founded in 2025, are actively disrupting the space with AI-native embedded protection. Their focus on climate-sensitive regions demonstrates how highly targeted, sensor-driven micro-insurance can scale profitably.

The Strategic Action Plan: Future-Proofing Risk Architecture

Strategic Trajectory

- Transition coverage models from natural disaster focus toward ‘Systemic Cyber’ and digital supply chain risk.

- Leverage server-uptime triggers to automate mitigation for global cloud outages.

- Deploy ‘Accountable AI’ frameworks to provide regulatory audit trails while managing autonomous underwriting.

- Integrate embedded parametric triggers as a standard feature across non-financial digital platforms.

- Target the projected $700 billion global opportunity value for on-demand insurance solutions by 2030.

To maintain a competitive edge, financial architects must look beyond localized weather anomalies and agricultural yields. The next 24 months will demand a strategic pivot toward systemic cyber risk and complex digital supply chain vulnerabilities. As global commerce becomes entirely reliant on cloud infrastructure, the cost of downtime scales exponentially.

Forward-thinking executives must leverage server-uptime triggers to mitigate the catastrophic financial impact of global cloud outages. By embedding parametric logic into digital service-level agreements, enterprises can automate financial recovery before the outage is even fully resolved.

Furthermore, the rise of accountable AI will be the critical bridge to widespread regulatory approval. These advanced machine learning models are designed to provide immutable, transparent audit trails for regulatory bodies. They manage multi-step underwriting entirely autonomously while maintaining strict compliance with evolving data sovereignty laws.

The Convergence of Decentralized Finance and Risk

The architectural foundation of future parametric models will inevitably intersect with decentralized finance protocols. Smart contracts deployed on public or enterprise blockchains offer the ultimate layer of trustless execution. This eliminates the counterparty risk traditionally associated with massive institutional payouts.

When a parametric trigger is activated, the smart contract can instantly route stablecoins directly to the insured corporate treasury. This bypasses the legacy correspondent banking network entirely. For multinational corporations managing cross-border supply chains, this capability ensures that liquidity is not trapped in sluggish international wire transfers.

Building API-First Embedded Protection

To capture the projected $700 billion global opportunity by 2030, FinTech founders must prioritize API-first architectures. The insurance product of the future will not be sold through a dedicated broker portal. Instead, it will be embedded directly into the user interface of software platforms, logistics dashboards, and agricultural management tools.

This requires a fundamental shift in how risk products are engineered from the ground up. They must be modular, highly scalable, and capable of ingesting millions of concurrent data points via RESTful APIs. The winners in this space will be the companies that make the complex mechanics of parametric underwriting entirely invisible to the end user.

Conclusion: The Algorithmic Future of Risk

The era of manual claims adjustment, prolonged investigations, and delayed indemnity is rapidly drawing to a close. Parametric and on-demand insurance models have definitively proven that liquidity can be engineered, automated, and deployed with algorithmic precision. We are witnessing the birth of a truly frictionless financial safety net.

As the Internet of Sensors expands its coverage and Agentic AI matures in its reasoning, the insurers of tomorrow will evolve. They will function less like traditional financial institutions and more like high-frequency trading firms. They will price risk dynamically, execute smart contracts instantly, and guarantee uninterrupted financial continuity for an increasingly volatile world.

Navigating the intersection of financial technology, institutional capital, and market psychology requires a sharp strategy. To future-proof your FinTech architecture and scale with precision, connect with Andres at Andres SEO Expert.

Frequently Asked Questions

What is the projected market size and growth for parametric insurance?

The global parametric insurance market is projected to reach $23.85 billion by 2026, growing at a compound annual growth rate (CAGR) of 13%. This growth is driven by institutional capital reallocation toward automated risk mitigation and a shift away from traditional indemnity models.

How does parametric insurance eliminate the indemnity gap?

Parametric insurance eliminates the indemnity gap by replacing subjective, manual loss assessments with objective, immutable triggers. Using real-time data from the Internet of Sensors and satellites, payouts are triggered automatically when predefined parameters are breached, providing instant liquidity without the need for traditional claims adjusters.

What is the impact of AI on insurance claims velocity?

AI significantly accelerates claims velocity by enabling straight-through processing. For example, Lemonade’s AI-driven platform now closes 40% of claims instantly. By late 2026, over 35% of global insurers are expected to use autonomous AI agents to reduce processing times by up to 70%.

Which region currently dominates the on-demand insurance market?

North America continues to dominate the on-demand insurance landscape, holding a 37.1% market share. This dominance is attributed to an established venture capital network and a regulatory environment that is increasingly receptive to algorithmic underwriting and automated risk platforms.

How do smart contracts and DeFi integrate with parametric insurance?

Smart contracts on blockchain networks provide a layer of trustless execution that eliminates counterparty risk. When a parametric trigger is activated, these contracts can instantly route stablecoins to the insured party’s treasury, bypassing legacy correspondent banking networks and international wire delays.

What is the future opportunity for embedded on-demand insurance?

The global opportunity for on-demand insurance solutions is projected to reach $700 billion by 2030. To capture this, FinTech providers are prioritizing API-first architectures that allow insurance triggers to be embedded directly into logistics dashboards, cloud service agreements, and agricultural management tools.