Key Points

- The transition to Agentic Action APIs transforms passive data-sharing into autonomous, machine-grade treasury and liquidity management.

- Institutional capital is aggressively targeting the invisible layers of embedded finance by funding stablecoin infrastructure and network-based fraud defense.

- Overcoming legacy integration debt requires adopting modular banking utilities to rapidly deploy full-stack lending and payment services.

Table of Contents

The Financial Tech Friction

The global financial ecosystem is undergoing a massive structural realignment driven by rapid technological adoption. Industry data projects the global fintech market will reach $460.76 billion by the end of 2026. This growth expands at a 16.2% CAGR as digital-first consumers in emerging markets fuel a shift away from traditional banking systems.

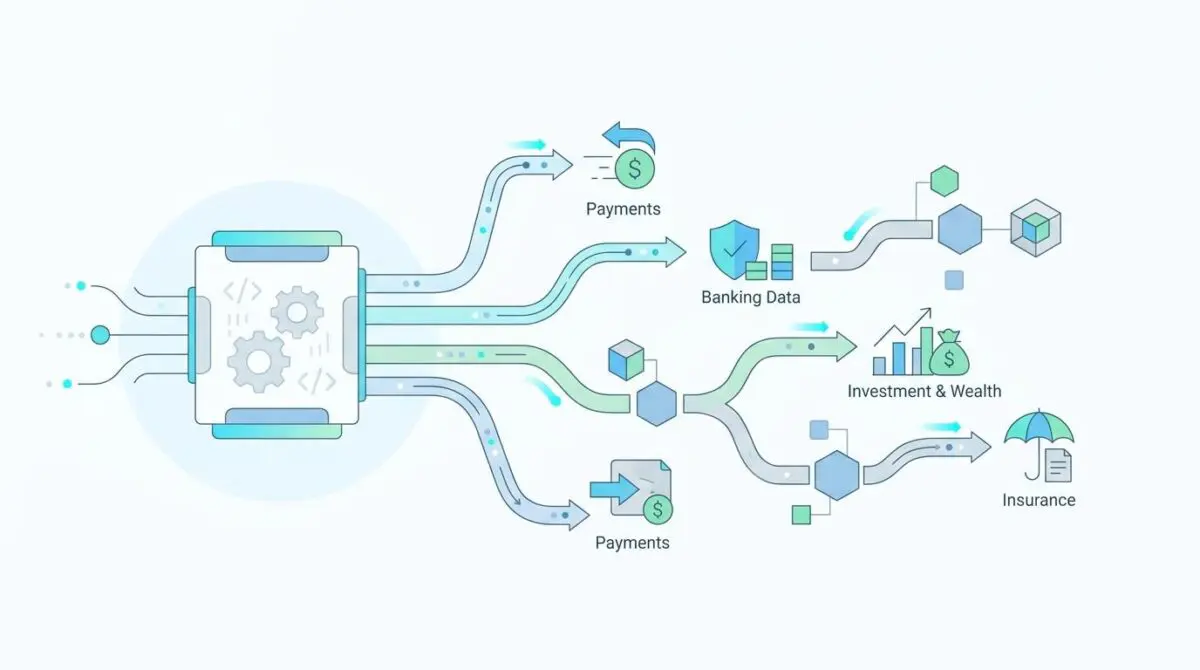

At the heart of this disruption lies a fundamental evolution in how financial services are built, scaled, and secured. We are moving rapidly from passive data-sharing mechanisms toward robust FinTech APIs and agentic infrastructure. This new paradigm treats financial capabilities as machine-grade services rather than human-facing tools.

Developers are now tasked with orchestrating autonomous AI agents that handle complex treasury rebalancing and real-time FX hedging. This requires identifying and integrating the most important FinTech APIs for developers to ensure seamless, scalable, and secure operations. The friction no longer stems from a lack of technology, but rather from the challenge of unifying multi-rail payments and decisioning engines into a single composable stack.

Market Intelligence and Capital Flow

Market Intelligence & Data

Embedded Finance Market

The global embedded finance market is expected to reach this valuation by the end of 2026, growing at a 21.8% CAGR according to Research and Markets.

Agentic AI Adoption

Data from the 2026 Global AI in Financial Services Report reveals that over half of industry respondents have already moved to active adoption of autonomous agentic AI.

API Call Volume

Annual open banking API calls are forecast by CoinLaw to surge to this level by 2029, a 7x increase from 2023 levels, driven by real-time payment initiations.

Stablecoin Settlements

Data published by FXC Intelligence indicates that stablecoin payment processing volumes reached this milestone in 2025, reflecting an 87% year-over-year jump.

The data clearly illustrates where the smart money is flowing across the global financial landscape. Institutional capital is aggressively targeting the invisible layers of the fintech stack, viewing infrastructure as the ultimate high-yield asset class. Global venture funding for these underlying technologies reached an astonishing $12 billion in the first quarter of 2026 alone.

This influx of capital is accelerating the development of agentic finance models and stablecoin infrastructure. Firms like Rain and BVNK are capturing significant market share, with the latter recently securing strategic backing from Citi Ventures. Investors understand that the future belongs to platforms capable of executing autonomous, cross-border liquidity movements at scale.

The Invisible Layers of FinTech Disruption

The era of simple RESTful calls is officially over, replaced by the necessity for Agentic Action APIs. These advanced interfaces allow developers to deploy autonomous agents capable of automated dispute resolution and dynamic risk management. A 2026 Gartner forecast predicts that more than 30% of the total increase in demand for financial APIs will be driven specifically by autonomous AI agents and LLM-based tools rather than traditional application interfaces.

This shift is creating a converged stack where AI decisioning, RTP, FedNow, and stablecoins operate in unified harmony. Market leaders like Plaid have already recognized this trajectory, pivoting heavily toward network-based fraud defense to secure these complex interactions. Meanwhile, AI-native challengers like Allica Bank and Mal are outperforming traditional incumbents by deploying specialized agentic crews to handle SME lending at unprecedented scale.

The integration of these technologies is heavily documented in the 2026 Global AI in Financial Services Report, which highlights the critical need for advanced decisioning models. Financial institutions that fail to adopt these invisible layers will find themselves unable to compete with the speed and accuracy of machine-driven lending and treasury management.

Agentic Crews and Network Defense

One of the most significant barriers to innovation has been legacy integration debt, which previously required 18-month lead times for new product launches. Modern FinTech APIs resolve this friction by providing Banking-as-a-Service as a modular, instantly deployable utility. This allows non-financial enterprises to embed full-stack lending and payment services instantly, effectively turning fixed operational costs into variable ones.

However, this rapid expansion of open banking networks introduces new vulnerabilities. The industry observed a staggering 181% surge in API-targeted fraud in 2025, necessitating a complete overhaul of security protocols. Infrastructure providers are now eliminating the friction of siloed KYC and AML data by enabling portable digital identities.

To handle the massive scale of these new systems, robust network defenses are non-negotiable. Industry analysts anticipate these automated open banking interactions will surge to over 720 billion by 2029, representing a sevenfold increase from recent baselines. Securing this volume requires biometric-native security APIs that can effectively replace legacy OAuth and 2FA protocols.

Intent-Based Banking and the Future

Over the next 12 to 24 months, the financial technology industry will evolve rapidly toward Intent-Based Banking. In this model, developers will no longer write code for specific, rigid transaction logic. Instead, they will define high-level business goals and parameters for AI agents to execute autonomously across fragmented global liquidity pools.

This evolution relies heavily on the widespread adoption of ISO 20022 messaging standards, ensuring that machine-to-machine communications are universally understood. As these autonomous financial calls begin to dominate total network volume by 2027, the underlying infrastructure must be highly composable and deeply resilient.

While regulatory frameworks continue to adapt to these autonomous systems, the primary focus for technical architects must remain on innovation and scalability. Ensuring that compliance checks are baked directly into the API layer allows agents to execute trades and settle payments without human intervention or regulatory breaches.

The Strategic Action Plan

Strategic Trajectory

- Pivot development roadmaps toward ‘Intent-Based Banking’ models within the next 12-24 months.

- Transition from hard-coded transaction logic to high-level business goal definitions for autonomous AI execution.

- Optimize API infrastructure for autonomous agent interactions across global liquidity pools.

- Implement biometric-native security protocols to phase out legacy OAuth and 2FA standards.

- Architect systems to handle the projected dominance of machine-to-machine financial call volume by 2027.

Executing this strategic trajectory requires a fundamental shift in how engineering teams approach financial architecture. Executives must prioritize the decoupling of legacy monolithic systems in favor of microservices that support agentic workflows. This modular approach ensures that organizations can swap out underlying payment rails or decisioning engines without disrupting the end-user experience.

Furthermore, investing in robust identity and access management is critical as machine-to-machine interactions become the primary driver of network traffic. By embracing biometric-native security and portable digital identities, firms can drastically reduce customer acquisition costs while fortifying their perimeters against sophisticated API-targeted attacks.

Conclusion

The shift toward agentic infrastructure represents the most significant technological leap in financial services since the advent of digital banking. By transforming complex financial capabilities into autonomous, machine-grade services, forward-thinking organizations can unlock unprecedented operational efficiency and scale.

Navigating the intersection of financial technology, institutional capital, and market psychology requires a sharp strategy. To future-proof your FinTech architecture and scale with precision, connect with Andres at Andres SEO Expert.

Frequently Asked Questions

What is agentic infrastructure in the context of modern FinTech?

Agentic infrastructure refers to a shift from human-facing financial tools to machine-grade services. It utilizes autonomous AI agents to orchestrate complex operations such as treasury rebalancing, real-time FX hedging, and automated dispute resolution via specialized Agentic Action APIs.

What are the growth projections for the global FinTech market by 2026?

The global FinTech market is projected to reach approximately $460.76 billion by the end of 2026, expanding at a CAGR of 16.2%. This growth is primarily fueled by digital-first consumers in emerging markets and the rise of embedded finance systems.

How is AI impacting the volume of financial API calls?

Driven by autonomous AI agents and real-time payment initiations, annual open banking API calls are forecast to surge to 720 billion by 2029. Gartner predicts that more than 30% of this demand will be generated specifically by autonomous AI agents and LLM-based tools.

What is Intent-Based Banking and why is it significant?

Intent-Based Banking is a model where developers define high-level business goals rather than rigid transaction logic. AI agents then execute these goals autonomously across global liquidity pools, utilizing ISO 20022 messaging standards to ensure universal machine-to-machine communication.

How is FinTech security evolving to combat API-targeted fraud?

To address a 181% surge in API-targeted fraud, the industry is transitioning toward biometric-native security APIs and portable digital identities. These modern protocols are designed to replace legacy OAuth and 2FA standards to better secure autonomous machine-to-machine interactions.

What role does ISO 20022 play in the future of autonomous finance?

ISO 20022 is the critical messaging standard that enables seamless machine-to-machine communication. It ensures that autonomous financial agents can operate across fragmented global liquidity pools with high-level business parameters that are universally understood and compliant.