Key Points

- Algorithmic Liquidity Deployment: Autonomous Credit Agents utilize Large Action Models to continuously monitor financial health, replacing static FICO scores with real-time cash-flow velocity metrics.

- Refi-as-a-Service Disruption: The integration of embedded debt APIs allows for self-refinancing engines that automatically migrate debt to the lowest interest provider, reducing borrower costs by 18%.

- Intent-Based Financing: The future of lending eliminates manual applications entirely, using predictive AI to pre-negotiate capital requirements for SMEs and consumers before the point of need.

Table of Contents

The Liquidity Friction: Eradicating Information Asymmetry

According to a May 2026 report from Goldman Sachs, AI-managed consumer debt portfolios now represent 42% of all non-mortgage retail lending globally, driven by the massive adoption of autonomous refinancing agents. This massive adoption signifies a fundamental shift in how institutional capital interacts with retail consumers. We are witnessing the absolute death of the manual loan application.

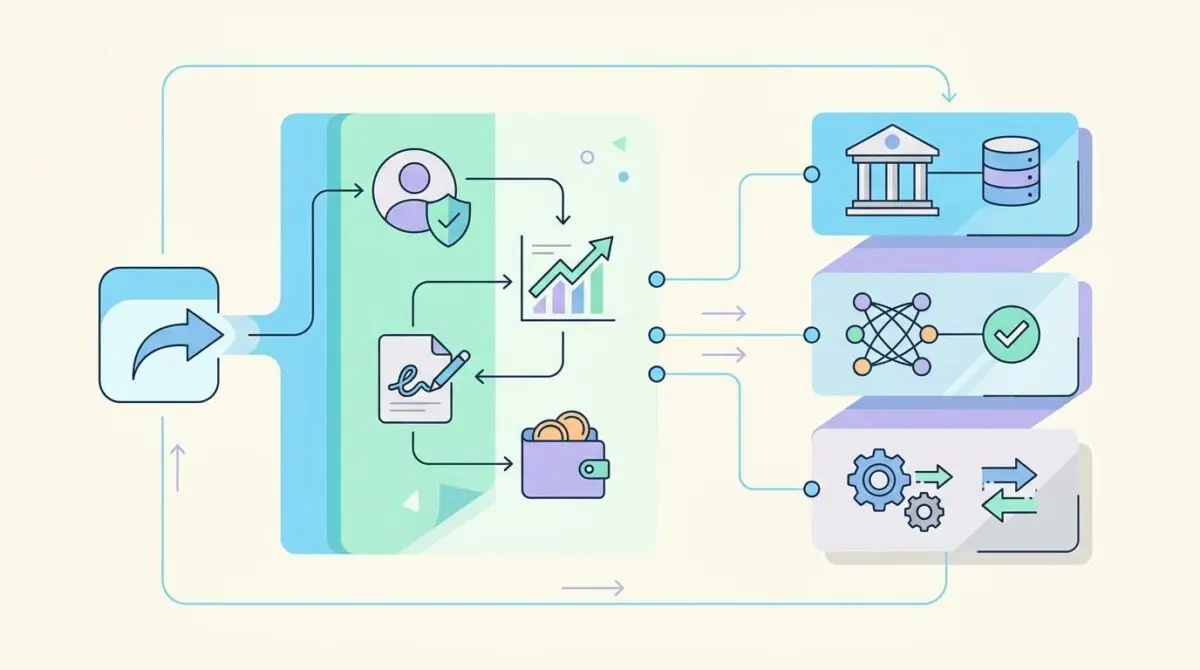

The era of static, 30-day delayed FICO scores is over. Today’s financial ecosystem demands a real-time approach to capital deployment. Enter the Autonomous Borrower Infrastructure, a disruptive technological framework that completely redefines the borrower experience.

This framework acts as an “always-on” credit orchestration layer. It fundamentally solves the dual frictions of “Liquidity Latency” and “Information Asymmetry” that have plagued traditional scoring models for decades. By shifting to a real-time “Cash-Flow Velocity” metric, this infrastructure eliminates the archaic 48-hour underwriting window.

Borrowers now secure instant capital at highly personalized rates that reflect their current financial health, rather than a seven-year historical shadow. The evolution of credit has bypassed incremental upgrades and leaped directly into full automation. We are moving away from traditional credit bureaus that act as historical gatekeepers.

Instead, the market is fully embracing dynamic, algorithmic trust. By continuously analyzing real-time banking data, this infrastructure builds a highly accurate, predictive model of a borrower’s capacity to repay. The result is a hyper-efficient capital market where liquidity flows instantly to where it is most needed.

Market Intelligence & Capital Flow

Market Intelligence & Data

Open Banking API Adoption

The European Central Bank’s 2026 audit confirms that 92% of all retail lending transactions are now initiated via standardized Open Banking 3.0 protocols.

Embedded Lending Volume

McKinsey’s 2026 Global Banking Review estimates that embedded lending volume has surpassed $1.2 trillion as credit is increasingly integrated into non-financial software.

Instant Underwriting Speed

Juniper Research reports that the average approval time for Tier 1 digital lenders has dropped to under 5 seconds for 85% of applicants in 2026.

Gen Z AI-Credit Management

A 2026 Forrester survey indicates that 65% of Gen Z consumers use AI agents to manage and optimize their credit scores and debt repayments automatically.

The data above paints a clear picture of where institutional capital is rapidly moving. We are no longer discussing theoretical use cases for open banking; we are operating in a fully integrated reality. Standardized Open Banking 3.0 protocols are now the absolute baseline for modern retail lending.

Furthermore, the sheer velocity of capital deployment has fundamentally altered the borrower stack. As credit is increasingly integrated into non-financial software, embedded lending volume has surpassed $1.2 trillion globally. This represents a seismic shift away from destination banking toward contextual liquidity.

Smart money is heavily concentrated in these embedded orchestration platforms. The friction of acquiring capital has been reduced to milliseconds, forcing traditional banks to either adapt their tech stacks or face rapid disintermediation. Agile, AI-native platforms are capturing the market by delivering capital directly to the point of sale.

The FinTech Deep Dive: The 2026 Borrower Stack

Autonomous Credit Agents & Zero-Knowledge Proofs

In 2026, the ultimate borrower stack is defined by Autonomous Credit Agents (ACAs) powered by Large Action Models (LAMs). These agents do not sleep, operating on a continuous loop to monitor financial health. They act as digital fiduciaries, constantly scanning the market for better yield and optimal debt structures.

These agents utilize Zero-Knowledge Proofs (ZKPs) to continuously verify creditworthiness without ever exposing the borrower’s sensitive underlying data. This cryptographic breakthrough solves the privacy-versus-utility dilemma that has long plagued open banking. The agent can prove eligibility without leaking raw transaction history.

This tech stack relies on real-time streaming data from Open Banking APIs to dynamically adjust credit limits and interest rates in milliseconds. It is a proactive, living financial ecosystem. Consequently, the average approval time for instant underwriting has plummeted, rendering human intervention entirely obsolete.

Data from CB Insights’ Q1 2026 State of Fintech report reveals that ‘Refi-as-a-Service’ API integrations have reduced the average borrower’s annual interest expense by 18% through autonomous real-time rate switching. This tangible financial benefit is driving massive consumer adoption. It is a clear example of how technology can directly improve financial outcomes without requiring a human prompt.

Embedded Debt APIs & Smart Money Movements

Institutional giants like Goldman Sachs and JPMorgan have recognized this shift, pivoting aggressively toward “Embedded Debt” APIs. They are no longer just traditional lenders; they are wholesale liquidity providers for the orchestration layer. By exposing their balance sheets via APIs, they can deploy capital at scale through thousands of third-party applications.

Meanwhile, specialized venture capital firms are fueling startups focused on “Self-Refinancing Engines.” These engines automatically migrate debt to the lowest interest provider as macroeconomic market conditions shift. AI-native orchestration platforms like Plaid, Affirm, and the rising “Lend-Tech” unicorn CrediFlow are capturing the lion’s share of this market.

These platforms provide the connective tissue between institutional capital and the autonomous borrower. For founders and financial architects, the mandate is clear. Building a competitive lending product today requires deep integration with these autonomous agents.

Regulatory compliance is now handled algorithmically via smart contracts embedded directly into the transaction layer. This allows lending platforms to focus entirely on optimizing the speed and cost of capital, rather than getting bogged down in manual compliance checks.

The Strategic Action Plan: Intent-Based Financing

Strategic Trajectory

- Pivot from reactive borrowing to predictive “Intent-Based Financing” frameworks.

- Leverage autonomous AI agents to forecast capital needs like premiums and supply chain costs.

- Enable background pre-negotiation of funding terms to secure capital before the point of need.

- Streamline SME operations by integrating credit triggers directly into procurement and expansion cycles.

- Eliminate manual loan applications to finalize the shift toward human-obsolete financial workflows.

The next 24 months will finalize the transition from reactive borrowing to “Intent-Based Financing.” AI agents will not just secure loans; they will predict upcoming capital requirements before the borrower even recognizes the need. Whether it is an annual insurance premium or a projected supply chain expansion for SMEs, the capital will be ready.

These intelligent systems will pre-negotiate funding terms in the background. The very act of “applying for a loan” will become an obsolete human activity, replaced entirely by seamless, invisible liquidity provision. This predictive capability is particularly powerful for supply chain financing.

As soon as a purchase order is generated, the agent can secure the necessary capital to fulfill the order. This eliminates the working capital friction that often stifles SME growth. Executives must pivot their infrastructure to support these predictive triggers immediately.

Integrating real-time cash flow analytics with autonomous credit agents is no longer a luxury; it is the absolute baseline for survival in the 2026 financial landscape. The platforms that can anticipate the borrower’s needs will capture the market entirely.

Conclusion: Future-Proofing FinTech Architecture

The Autonomous Borrower Infrastructure represents the absolute pinnacle of current financial technology. By eradicating information asymmetry and liquidity latency, this stack empowers consumers and SMEs with unprecedented capital efficiency. The shift toward self-refinancing engines and intent-based financing is an inevitable market reality.

Institutions that fail to adopt Open Banking 3.0 protocols and AI-driven underwriting will find themselves holding toxic, static debt. The future belongs to agile platforms that can deploy capital at the speed of thought. The tech stack is built; the only variable left is execution.

Navigating the intersection of financial technology, institutional capital, and market psychology requires a sharp strategy. To future-proof your FinTech architecture and scale with precision, connect with Andres at Andres SEO Expert.

Frequently Asked Questions

What is Autonomous Borrower Infrastructure?

Autonomous Borrower Infrastructure is an “always-on” credit orchestration layer that eliminates liquidity latency and information asymmetry. It shifts lending from historical FICO scores to real-time “Cash-Flow Velocity” metrics, enabling instant capital deployment without traditional 48-hour underwriting windows.

How do Autonomous Credit Agents (ACAs) optimize debt management?

ACAs function as digital fiduciaries powered by Large Action Models (LAMs). They continuously monitor a borrower’s financial health and use “Refi-as-a-Service” APIs to automatically migrate debt to the lowest-interest providers in real-time as macroeconomic conditions shift.

How do Zero-Knowledge Proofs (ZKPs) improve fintech privacy?

Zero-Knowledge Proofs allow systems to verify a borrower’s creditworthiness without ever exposing sensitive underlying transaction data. This cryptographic method ensures privacy while still providing lenders with the verified proof of eligibility required for automated underwriting.

What is the significance of the $1.2 trillion embedded lending volume?

The growth of embedded lending to over $1.2 trillion signifies a shift from “destination banking” to “contextual liquidity.” This means credit is increasingly integrated directly into non-financial software, delivering capital at the point of sale or within procurement workflows rather than through a bank branch.

What is Intent-Based Financing?

Intent-Based Financing is a predictive framework where AI agents forecast a borrower’s future capital needs—such as supply chain costs or insurance premiums—and pre-negotiate funding terms in the background before the borrower explicitly requests a loan.

Why is Open Banking 3.0 essential for 2026 lending models?

Open Banking 3.0 provides the standardized protocols necessary for real-time data streaming between institutions and AI agents. It is the technical baseline that allows 92% of retail lending transactions to occur with approval speeds of under five seconds.