Key Points

- Robo-advisory platforms are transitioning to “Agentic Wealth Management,” utilizing multimodal LLMs to offer conversational financial planning and predictive behavioral coaching.

- Direct indexing has become a standard feature, allowing both beginners and experienced investors to capture significant tax alpha and hyper-efficient tax-loss harvesting.

- The industry is moving toward a “Self-Driving Money” model, evolving digital platforms from simple portfolio managers into holistic, autonomous Chief Financial Officers for individuals.

Table of Contents

The Financial Tech Friction: Breaking the Wealth Gap

The era of static, set-it-and-forget-it portfolios is officially dead. In its place, a new breed of financial technology is actively reshaping how capital is deployed, protected, and grown.

We are entering a phase where autonomous systems dictate the velocity of money. As of May 2026, global assets under management within robo-advisory platforms have scaled to $5.3 trillion. This staggering milestone is largely driven by a massive surge in Gen Z adoption since 2024.

The institutional landscape is taking notice of this massive liquidity shift. We are witnessing the rapid evolution of the best robo-advisors for beginners and experienced investors. These platforms eliminate historical wealth gap friction by providing sophisticated asset-allocation strategies.

Previously, these quantitative tools were exclusively reserved for ultra-high-net-worth clients with massive capital reserves. For beginners, this technology solves the psychological barrier of analysis paralysis. It achieves this through automated recurring deposits and intelligent behavioral nudges that prevent emotional selling.

The system acts as a rational anchor during periods of intense market volatility. For experienced investors, it resolves the operational complexity of managing multi-asset class diversification. In a volatile, high-interest-rate environment, manual portfolio balancing is a mathematical disadvantage.

Algorithms execute these adjustments with zero latency and absolute precision. The democratization of elite financial strategies is now a mathematical reality.

Market Intelligence & Capital Flow

Market Intelligence & Data

Direct Indexing Adoption

The percentage of experienced investors now utilizing robo-platforms for direct indexing to capture tax-alpha, according to 2026 data from Cerulli Associates.

AI-Wealth Tech Funding

Total venture capital injected into AI-first wealth management startups in Q1 2026 alone, as reported by the Financial Times.

Average Fee Compression

The new competitive floor for basic automated management fees among top-tier digital advisors in 2026, per Morningstar’s annual fee study.

Mobile-First Execution

The share of all robo-advisory trades executed via voice-activated AI or mobile interfaces in 2026, according to a report from J.P. Morgan Asset Management.

Analyzing the Data

The numbers reveal a massive shift in how smart money flows through digital ecosystems. Institutional capital is aggressively backing AI-first wealth management startups. This signals a permanent departure from traditional, human-centric advisory models.

Much of this momentum is captured in the broader Global Wealth Report by Statista, which highlights the explosive growth in digital-first asset management. As retail liquidity pools deepen, the competitive landscape is forcing legacy institutions to adapt. Failure to innovate in this space practically guarantees obsolescence.

Furthermore, fee structures are experiencing unprecedented pressure across the industry. The new competitive floor for basic automated management fees among top-tier digital advisors is now 12 basis points. This metric is heavily analyzed in recent annual fee studies across the financial sector.

This fee compression is not merely a race to the bottom. Instead, it represents a pivot toward highly specialized, value-added services. Platforms are now competing on algorithmic superiority, hyper-personalized tax efficiency, and frictionless user experiences.

The FinTech Deep Dive: From Automation to Autonomy

Direct Indexing and Tax Alpha Engineering

The technological landscape has pivoted sharply from basic automated rebalancing. The new frontier is what industry insiders call agentic wealth management. Cutting-edge platforms now utilize multimodal Large Language Models to provide real-time financial guidance.

This conversational financial planning allows retail investors to interact with their portfolios using natural language. It bridges the gap between complex quantitative analysis and everyday financial literacy. The AI explains market movements in simple, actionable terms.

Innovation is currently dominated by direct indexing for the masses. This disruptive tech allows retail investors to own individual securities within a broader index. It completely bypasses the limitations of traditional mutual funds or rigid ETFs.

By holding the underlying assets directly, the platform unlocks hyper-efficient tax-loss harvesting. This generates significant tax alpha, systematically offsetting capital gains with harvested losses. The algorithm scans the portfolio daily to execute these micro-trades automatically.

Recent industry analyses reveal that robo-advisors incorporating predictive sentiment analysis have significantly reduced client churn. By adjusting portfolio risk based on a user’s real-time spending stress levels, these platforms prove that emotional intelligence can be seamlessly coded into financial algorithms.

AI-Native Disruptors vs. Legacy Titans

Market dominance is currently split between AI-native startups and legacy financial titans. Leading digital platforms have evolved far beyond simple investment applications. They are rapidly transforming into full-stack autonomous banks.

Conversely, legacy institutions have integrated deep-learning analytics directly into their retail interfaces. This hybrid approach marries institutional-grade risk management with consumer-friendly accessibility. It brings Wall Street computing power directly to Main Street smartphones.

Significant venture capital is also flowing into cross-border robo-advisory startups. These platforms automatically navigate multi-currency tax jurisdictions. They perfectly serve a growing demographic of digital nomads and borderless global citizens.

From a regulatory standpoint, these platforms must navigate complex global compliance frameworks. Ensuring cross-border data privacy and algorithmic transparency requires rigorous legal engineering. However, the primary focus remains on leveraging technology to outpace these regulatory hurdles through automated compliance reporting.

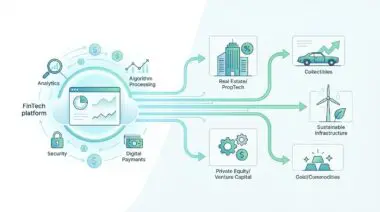

The Real-World Asset Integration

Additionally, we are seeing the rise of niche platforms targeting high-net-worth creators and gig-economy professionals. These platforms integrate tokenized private equity and real-world assets into standard risk-parity portfolios. This effectively democratizes alternative investments that were previously locked behind institutional gates.

The integration of Real-World Assets marks a critical evolution in robo-advisory platforms. By tokenizing private credit, real estate, and infrastructure, algorithms can fractionalize massive illiquid markets. This allows retail capital to flow into high-yield environments seamlessly.

Smart contracts execute the distribution of yields directly into the user’s automated portfolio. This eliminates the need for manual fund transfers or complex brokerage approvals. The blockchain layer operates invisibly beneath a sleek, intuitive user interface.

This convergence of decentralized finance and traditional robo-advisory creates a frictionless liquidity loop. Capital never sits idle; it is constantly hunting for the optimal risk-adjusted return. The machine ensures that every dollar is deployed with maximum efficiency.

The Psychology of Automated Wealth

Engineering Behavioral Guardrails

One of the most profound innovations in modern wealth tech is the coding of behavioral psychology into trading algorithms. Human investors are notoriously prone to panic selling during market corrections. Automated platforms neutralize this biological flaw through engineered friction.

When a user attempts to liquidate assets during a market dip, the system deploys conversational AI to provide immediate context. It instantly calculates the projected long-term loss of compounding interest caused by the withdrawal. This micro-intervention forces the user to confront the mathematical reality of their emotional decision.

By acting as a rational buffer, the platform preserves capital that would otherwise be destroyed by panic. This is where the true value of agentic wealth management shines. The algorithm actively protects the investor from their own worst instincts.

The Gamification of Yield

Beyond defense, these platforms are mastering the psychology of wealth accumulation through positive reinforcement loops. The gamification of yield encourages users to increase their savings rate organically. Visualizing compounding interest in real-time triggers dopamine responses traditionally associated with consumer spending.

This psychological rewiring transforms passive savers into aggressive capital allocators. As users watch their automated micro-deposits snowball into significant holdings, their engagement with the platform deepens. It creates an incredibly sticky user base with exceptionally high lifetime value.

The Strategic Action Plan: Self-Driving Money

Strategic Trajectory

- Operationalize ‘Self-Driving Money’ protocols to move beyond portfolio management toward holistic balance sheet control.

- Implement AI-driven debt refinancing modules to automatically optimize individual liability structures.

- Establish automated capital liquidity flows into high-yield Real-World Asset (RWA) vaults.

- Embed predictive tax filing integrations to streamline fiscal compliance within the investment interface.

- Pivot organizational identity from ‘Robo-Advisor’ to ‘Autonomous Chief Financial Officer’ for the individual consumer.

Executing the Vision

The near future will usher in the highly anticipated era of self-driving money. Robo-advisors are moving rapidly beyond standard investment portfolios. They are being engineered to manage a consumer’s entire balance sheet simultaneously.

Founders and product architects must prioritize AI-driven debt refinancing modules. These systems automatically analyze a user’s liabilities and seamlessly transition them to lower-interest credit facilities. It optimizes the liability side of the ledger just as aggressively as the asset side.

Furthermore, predictive tax filing integrations will streamline fiscal compliance within the investment interface. By forecasting tax liabilities in real-time, the platform can adjust its harvesting strategies proactively. It eliminates the end-of-year tax scramble entirely.

Ultimately, the industry is shifting its core organizational identity. The successful platforms of tomorrow will no longer be known merely as robo-advisors. They will be universally recognized as the autonomous chief financial officer for the individual consumer.

Conclusion

The transformation of robo-advisory platforms represents one of the most significant wealth creation events in modern financial history. By replacing friction with autonomous intelligence, these platforms are redefining what it means to build and protect wealth.

For institutions and retail investors alike, the mandate is abundantly clear. You must adapt to agentic wealth management or risk being left behind in a rapidly accelerating digital economy. The future of finance belongs to those who embrace algorithmic autonomy.

Navigating the intersection of financial technology, institutional capital, and market psychology requires a sharp strategy. To future-proof your FinTech architecture and scale with precision, connect with Andres at Andres SEO Expert.

Frequently Asked Questions

What are the best robo-advisors for beginners and experienced investors in 2026?

In 2026, market dominance is split between AI-native platforms like Wealthfront and Betterment and legacy titans like Vanguard and BlackRock. For beginners, the best options focus on automated recurring deposits and behavioral nudges, while experienced investors prioritize platforms offering direct indexing, Aladdin-grade analytics, and multi-asset diversification.

How does direct indexing generate tax alpha in automated portfolios?

Direct indexing allows retail investors to own individual securities within an index rather than a rigid ETF. This enables algorithms to execute hyper-efficient, daily tax-loss harvesting by selling specific underlying assets at a loss to offset capital gains, systematically increasing the portfolio’s after-tax return, or “tax alpha.”

What is the average fee for robo-advisory services in 2026?

According to the 2026 Morningstar fee study, unprecedented fee compression has pushed the competitive floor for basic automated management to 12 basis points (0.12%). This shift reflects a pivot toward platforms competing on specialized value-add services like algorithmic superiority rather than just basic portfolio rebalancing.

How do AI-driven platforms prevent emotional selling during market volatility?

Modern wealth tech utilizes “agentic wealth management” to act as a rational buffer. When investors attempt to liquidate during market dips, the system deploys conversational AI to calculate and display the projected long-term loss of compounding interest, creating engineered friction that forces a confrontation with mathematical reality over emotional impulse.

What is the role of Real-World Assets (RWA) in modern robo-advisory?

Robo-advisors now integrate tokenized real-world assets like private credit, real estate, and infrastructure into standard risk-parity portfolios. This democratization allows retail capital to flow into high-yield, previously illiquid institutional markets, with smart contracts executing yield distributions directly into the user’s automated portfolio.

What does the term “self-driving money” mean in financial technology?

Self-driving money refers to the evolution of robo-advisors into autonomous chief financial officers. These systems manage an individual’s entire balance sheet, including automated debt refinancing, predictive tax filing, and real-time capital allocation across both assets and liabilities without manual user intervention.