Key Points

- Real-Time Defense: Event-driven Geofencing & Card Authorization Orchestration (EG-CAO) eliminates the fraud latency gap by instantly blocking compromised cards based on precise geolocation mismatches.

- Cognitive AI Integration: Legacy rule-based systems are being replaced by cognitive agents that utilize Retrieval-Augmented Generation to instantly compare GPS signals against historical travel profiles.

- Frictionless Customer Experience: Automated push-notification loops allow legitimate users to instantly override false positives via biometric authentication, preventing the dreaded stranded traveler scenario.

Table of Contents

- The Silent Drain of the Fraud Latency Gap

- The Escalating Financial Toll of Physical Skimming

- Balancing Proximity Verification with Consumer Privacy

- Contextualizing Travel Profiles with Cognitive Agents

- Curing the Stranded Traveler Syndrome via Push Loops

- Overcoming Battery Saver Mismatches and Logic Fallbacks

- Eradicating the Operational Burnout of Dispute Management

- The Impending Shift Toward Mesh Verification and Proof of Presence

- Pioneering the Next Era of Dynamic Authorization

The Silent Drain of the Fraud Latency Gap

Imagine a business traveler enjoying coffee at a JFK Airport terminal. They are completely unaware that their cloned credit card is simultaneously being swiped at a gas station in Eastern Europe.

This scenario perfectly illustrates the fraud latency gap. It is a critical vulnerability where manual card-blocking protocols fail miserably. By the time a human analyst reviews a suspicious transaction flag, thousands of dollars have already vanished.

Legacy banking infrastructure relies heavily on reactive dispute management rather than proactive prevention. This outdated approach creates massive operational bottlenecks. It also leaves consumers exposed to increasingly sophisticated physical skimming networks.

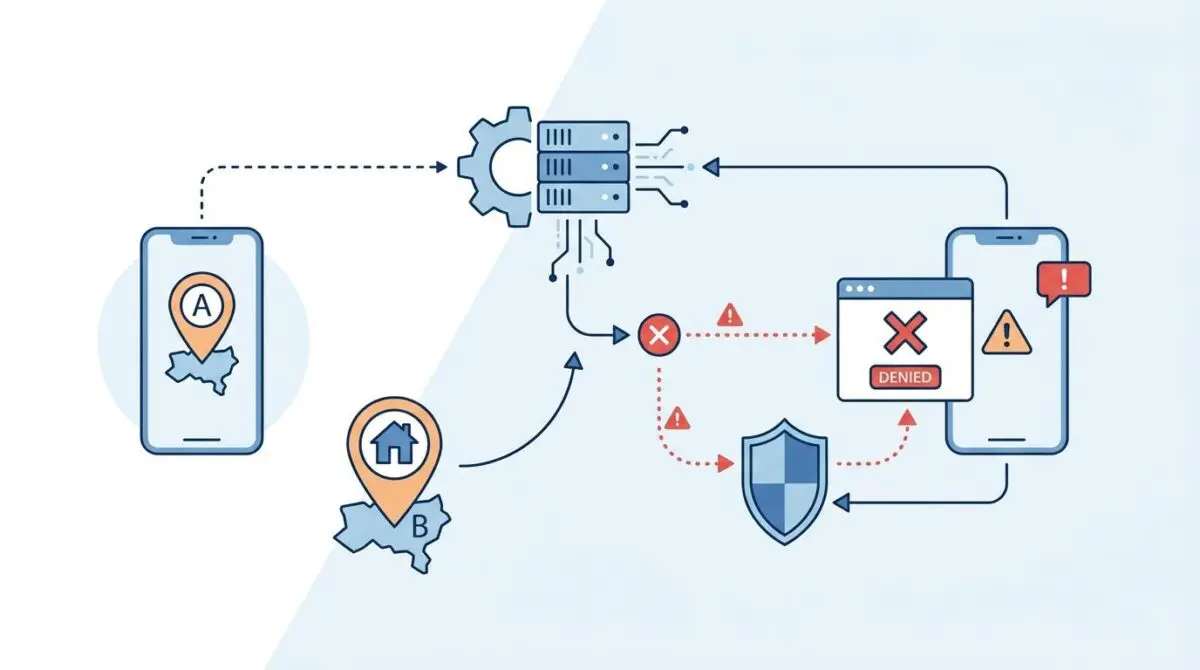

The ultimate solution to this hemorrhaging of capital is Event-driven Geofencing and Card Authorization Orchestration (EG-CAO). Institutions can integrate mobile app location data directly with core banking authorization engines. This allows them to trigger automated transaction blocks the millisecond a geographic mismatch occurs.

The Escalating Financial Toll of Physical Skimming

Market Intelligence & Data

Fraud Prevention Market 2026

According to a June 2026 market report by Fortune Business Insights, the global fraud detection and prevention market reached this valuation as real-time payment automation became a mandatory banking standard.

Surge in Card Skimming

A 2026 FICO report highlighted that card skimming attacks surged by 90% in 2025, driving the urgent adoption of geolocation-triggered kill switches to mitigate physical card cloning.

Reduction in Detection Time

Financial institutions employing AI-driven orchestration witnessed up to a 50% reduction in fraud detection and response times compared to 2023 levels, according to 2025 data from Feedzai.

Card-Not-Present Losses

A 2026 Chargebacks911 study estimates that annual global losses from card-not-present fraud have climbed to this level, representing a 40% increase from 2023.

The staggering $40.4 billion valuation of the fraud prevention market underscores a massive industry shift away from manual oversight. As detailed in the Fortune Business Insights global fraud detection and prevention market report, institutions are aggressively investing in automated orchestration layers. This capital influx proves that real-time payment automation is now a baseline requirement for survival.

This urgency is directly fueled by an alarming 90% surge in physical card skimming attacks. Criminal syndicates have weaponized miniaturized hardware to bypass traditional visual inspections at point-of-sale terminals. Consequently, banks must rely on automated geolocation-triggered kill switches to outpace these sophisticated cloning operations.

Fortunately, deploying AI-driven orchestration yields tangible operational victories. Institutions report up to a 50% reduction in fraud detection and response times. By removing human hesitation from the authorization loop, banking systems can instantly cross-reference a card swipe with a mobile device location.

This velocity is the only proven method to intercept a fraudulent authorization request before funds clear the merchant gateway. However, handling sensitive mobile location data requires rigorous security measures to prevent breaches. Banks must adhere to the official PCI DSS 4.0.1 standard to ensure automated handshakes remain fully encrypted.

Balancing Proximity Verification with Consumer Privacy

One of the most complex hurdles in deploying EG-CAO is the inherent conflict between real-time location tracking and consumer privacy rights. Users want the security of instant fraud blocking. However, they rightfully reject the idea of their bank storing a persistent map of their daily movements.

To solve this, modern banking architectures utilize differential privacy filters that comply with strict GDPR mandates. By integrating identity platforms like Auth0 and Okta, the mobile-to-core-banking handshake is highly secured. This process relies on tokenized data exchanges rather than raw coordinate sharing.

Leading-edge banking apps now utilize Secure Enclave Local Inference to protect consumer data. This allows the user device to process geolocation mismatches internally and only send a simple boolean match signal to the bank. This brilliant engineering prevents the transmission of raw GPS data entirely while maintaining real-time security.

Contextualizing Travel Profiles with Cognitive Agents

Legacy rule-based fraud systems suffer from a severe lack of nuance. Their inability to distinguish between a fraudulent cross-border swipe and a legitimate layover results in a high volume of false positives.

Today, cognitive agents are rewriting the rules of engagement for financial institutions. These advanced AI entities utilize Retrieval-Augmented Generation to inject deep context into every single transaction.

When a transaction occurs, the AI instantly compares real-time GPS signals against the historical travel profile of the user. If a user frequently travels through specific international hubs, the orchestration layer intelligently approves the transaction. Hard blocks are reserved strictly for genuinely anomalous geographic deviations.

Curing the Stranded Traveler Syndrome via Push Loops

Aggressive automated blocking logic often triggers the dreaded stranded traveler syndrome. This occurs when a legitimate user is left entirely without funds in a foreign jurisdiction because an algorithm flagged an authentic purchase.

To eradicate this massive friction point, institutions are engineering advanced customer experience automation workflows. By utilizing modern communication APIs, banks can initiate instant push-notification loops the moment a transaction is paused.

These automated loops allow the user to immediately override and unblock the flagged transaction directly from their lock screen. By requiring a quick biometric confirmation, the system ensures the genuine cardholder remains in control. This transforms a potentially disastrous customer service failure into a seamless security feature.

Overcoming Battery Saver Mismatches and Logic Fallbacks

Automation relies on consistent data, but mobile devices are inherently unpredictable environments. A common pitfall in EG-CAO workflows is the failure node created when a phone enters battery saver mode.

When background app refresh is disabled to conserve power, the banking app cannot broadcast its current location. If the user then swipes their card, the system registers a false geolocation mismatch. This triggers an unintended and highly frustrating account block.

To mitigate this issue, robust orchestration workflows require intelligent logic fallbacks. When precise GPS data is unavailable, the system automatically defaults to an IP-based city-level resolution as a secondary check. This layered approach ensures that power management settings never paralyze consumer purchasing power.

Eradicating the Operational Burnout of Dispute Management

The hidden tax of manual fraud investigation is staggering for modern banks. It costs financial institutions an average of $110 to $150 per individual case. Human analysts are forced to dig through transaction logs, cross-reference IP addresses, and interview frustrated customers.

This reactive process leads to severe operational burnout and artificially inflates labor costs. Managing thousands of fraudulent chargeback disputes manually is simply not a scalable business model in the digital economy.

Implementing EG-CAO directly attacks this inefficiency by stopping fraud before the dispute phase even exists. Automation reduces the volume of obvious fraud calls to support centers by up to 70 percent. This frees up human analysts to investigate highly complex, syndicated fraud rings instead of routine skimming cases.

The Impending Shift Toward Mesh Verification and Proof of Presence

Looking toward the near future, the concept of a single device dictating authorization will become obsolete. The financial industry is rapidly shifting toward mesh verification. This highly secure paradigm demands multiple points of proximity to approve a transaction.

Under this new framework, a physical card will only remain active if the smartphone, smartwatch, and merchant terminal all report physical proximity simultaneously. This multi-device triangulation creates an irrefutable proof of presence.

This evolution addresses the critical single-point-of-failure risk where a user loses their phone but retains their physical card. Dynamic authorization will soon replace binary card blocking entirely. Systems will prompt for a real-time biometric heartbeat detected near the terminal to ensure absolute transactional integrity.

Pioneering the Next Era of Dynamic Authorization

The integration of Event-driven Geofencing and Card Authorization Orchestration is not just a security upgrade. It is a fundamental redesign of how trust is verified in real-time. By bridging the gap between physical location and digital authorization, institutions can finally outpace modern financial crime.

As we move toward a future defined by cognitive agents and mesh verification networks, reliance on manual human intervention will vanish entirely. The financial ecosystems that survive will be those embracing frictionless, invisible security protocols. These systems will protect capital without punishing the consumer.

Navigating the intersection of technology, workflows, and operational efficiency requires a sharp strategy. To future-proof your business architecture and scale with precision, connect with Andres at Andres SEO Expert.

Frequently Asked Questions

What is the fraud latency gap in banking?

The fraud latency gap is the critical time window between a fraudulent transaction and the manual intervention required to block it. Legacy banking systems often rely on reactive dispute management, which allows criminals to drain accounts before an analyst can review the flag. Automated orchestration layers like EG-CAO eliminate this delay by triggering instant blocks based on real-time data.

How does Event-driven Geofencing & Card Authorization Orchestration (EG-CAO) work?

EG-CAO integrates a user’s mobile device location data directly with the bank’s core authorization engine. When a card is swiped, the system instantly cross-references the merchant’s location with the user’s smartphone GPS. If a geographic mismatch is detected, the transaction is automatically paused or blocked within milliseconds to prevent losses from physical card skimming.

How do banks balance transaction security with user location privacy?

Modern banking architectures utilize Secure Enclave Local Inference and differential privacy filters. This allows a user’s smartphone to process geolocation mismatches internally and only transmit a tokenized “Match” or “No Match” boolean to the bank. This method ensures compliance with GDPR and PCI DSS 4.0.1 by protecting raw GPS coordinates from being stored or exposed.

What is the Stranded Traveler syndrome in automated fraud detection?

Stranded Traveler syndrome occurs when a legitimate user’s transaction is incorrectly flagged and blocked in a foreign location, leaving them without funds. To solve this, banks use CX automation workflows and communication APIs to send instant push notifications, allowing the cardholder to provide biometric confirmation (like FaceID) to immediately override the block and authorize the purchase.

What role do cognitive agents play in reducing false positives?

Cognitive agents use Retrieval-Augmented Generation (RAG) and AI to inject historical context into every transaction. Instead of using rigid rules, these agents analyze a user’s travel history and profile. If a user frequently travels through specific international hubs, the system intelligently approves the transaction, reducing friction for the consumer while maintaining high security for anomalous activities.

What is Mesh Verification and Proof of Presence in financial security?

Mesh Verification is an advanced security paradigm that requires multiple devices—such as a smartphone, smartwatch, and the merchant terminal—to report physical proximity simultaneously. This creates a multi-device triangulation known as Proof of Presence, ensuring that a physical card cannot be used unless the authorized user and their verified devices are physically present at the point of sale.