Key Points

- Decision Intelligence Finance: AI-driven credit scoring and spectral satellite imagery have replaced physical collateral, dropping agricultural interest rates from predatory levels to institutional baselines.

- Embedded Procurement Liquidity: Platforms are seamlessly integrating input financing and blockchain-based warehouse receipt financing directly into the daily operational workflows of agribusinesses.

- Autonomous Farm Wallets: The imminent shift toward Machine-to-Machine (M2M) payments and Regenerative Finance (ReFi) will allow autonomous machinery to execute DeFi transactions and tokenize carbon data in real time.

Table of Contents

- The Financial Tech Friction: Rewriting the Rules of Agricultural Liquidity

- Market Intelligence & Capital Flow: The Liquidity Migration

- The FinTech Deep Dive: Architecting Decision Intelligence Finance

- The Strategic Action Plan: Preparing for Autonomous Farm Wallets

- Conclusion: The Future of Smart Agricultural Money

The Financial Tech Friction: Rewriting the Rules of Agricultural Liquidity

According to data from ResearchAndMarkets, the global AgriFinTech market reached a valuation of $7.29 billion in 2024 and is projected to surge to $64.69 billion by 2035. This exponential growth is not merely a byproduct of general digitization. It represents a fundamental rewiring of how global capital interacts with biological risk.

For decades, traditional financial institutions viewed agriculture as a high-risk, opaque black box. The primary friction was a massive information asymmetry between the farmer and the underwriter. Banks simply could not accurately predict crop yields, soil health, or micro-climate weather patterns.

Because traditional lenders lacked the technological infrastructure to underwrite biological variables, they relied exclusively on physical land titles as collateral. This archaic requirement systemically excluded millions of smallholder farmers and modern agribusinesses operating on leased land. It ultimately forced agricultural operators into the shadow economy of predatory lending.

Today, the AgriFinTech ecosystem has emerged as the ultimate solution to this historical friction. It is a sophisticated network of digital platforms, alternative data streams, and decentralized ledgers designed to translate farming operations into verifiable financial metadata. By doing so, it unlocks unprecedented liquidity for the global food supply chain.

Market Intelligence & Capital Flow: The Liquidity Migration

The flow of institutional capital reveals a clear mandate. Smart money is aggressively hunting for yield in sectors where technology can eliminate legacy operational friction.

Market Intelligence & Data

Platform Market Valuation

The global agritech platform market is expected to reach this value by late 2026 as farmers migrate to unified data orchestration layers, according to Persistence Market Research.

Parametric Insurance Growth

The parametric insurance sector is projected to hit this milestone in 2026, driven by corporate demand for automated climate-risk payouts, as reported by Global Market Insights.

Quarterly VC Inflow

Despite a massive capital concentration in general AI, AgTech startups successfully secured this amount in venture funding during Q1 2026 alone, per CropLife data.

Digital Lending Dominance

Digital lending now represents the largest individual segment of the AgriFinTech solution market, according to 2025/2026 industry analysis from Dataintelo.

This data highlights a critical transition. Farmers and agribusinesses are rapidly migrating away from fragmented legacy software. They are adopting unified data orchestration layers that consolidate their operations, agronomy, and finances into a single pane of glass.

This consolidation is highly lucrative for FinTech architects. In fact, this foundational platform layer is expected to reach $18.9 billion by late 2026. When a platform controls the operational data of a farm, it inherently becomes the most qualified entity to offer financial products to that business.

Venture capital is acutely aware of this dynamic. The massive inflow of funding into specialized scale-ups demonstrates that the market is prioritizing verticalized FinTech solutions over generalized banking products. The AgriFinTech ecosystem is officially moving from the fringes of AgTech into the core of global financial services.

The FinTech Deep Dive: Architecting Decision Intelligence Finance

As we navigate through the current economic cycle, agricultural finance has officially transitioned from manual processing to what industry architects call Decision Intelligence Finance. This represents the seamless integration of predictive analytics, real-time data feeds, and automated capital deployment.

Eradicating Information Asymmetry

Leading AgriFinTech tools now integrate spectral satellite imagery with AI-driven credit scoring. This technology continuously monitors crop health, soil moisture, and photosynthetic activity from space. The AI engine then translates these biological metrics into a dynamic credit score.

This breakthrough provides instant, collateral-free liquidity to agribusinesses. By converting soil health and yield predictions into financial metadata, AgriFinTech tools completely bypass the need for physical land titles. The farm’s data effectively becomes its collateral.

The economic impact of this technological shift is staggering. These digital-first platforms have successfully reduced agricultural interest rates from predatory levels, which historically hovered between 36 and 60 percent. Today, data-rich farmers can access competitive institutional rates of approximately 12 percent.

Institutional capital is aggressively flowing into specialized scale-ups that bridge this gap between biological data and financial risk. Notable disruptors are securing massive funding rounds to expand revolutionary financial models. These innovations are effectively tokenizing agricultural assets into liquid financial instruments.

Embedded Finance and Smart Contracts

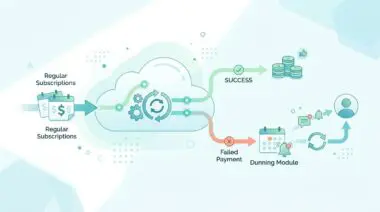

Another major pillar of Decision Intelligence Finance is embedded lending. Innovation is now heavily centered on embedded finance within agribusiness marketplaces. Digital platforms are leading this charge by integrating financial services directly into daily operational tools.

These platforms seamlessly bundle input financing, crop insurance, and real-time payments directly into the procurement workflow. When a farmer purchases seeds or fertilizer through an app, the financing is approved and executed in the background within milliseconds.

Furthermore, blockchain-based smart contracts are fundamentally disrupting inventory financing. They are now being used extensively for warehouse receipt financing. This allows farmers to unlock capital immediately upon grain storage.

The mechanism is elegant and trustless. IoT-enabled sensors verify the volume and quality of the inventory inside the silo. This verifiable data triggers a smart contract on a decentralized ledger, instantly releasing institutional funds to the farmer’s digital wallet without requiring a manual bank inspection.

Parametric Insurance Disruption

While lending provides the fuel for agricultural growth, insurance provides the safety net. However, traditional crop insurance was plagued by slow, manual loss-adjustment processes. This friction is being eliminated by tech-centric insurers deploying advanced digital models.

These major players are dominating the space by deploying parametric insurance models. Instead of sending an adjuster to inspect a flooded field, these models use hyper-local weather data and satellite feeds to trigger automatic payouts. If a specific weather threshold is breached, the smart contract executes the payment instantly.

This automated data-trigger system is accelerating claim settlement times by 30 to 40 percent. The efficiency and reliability of this model are so profound that the parametric insurance sector is projected to hit $22.6 billion in 2026.

A major institutional shift recently saw leading agricultural finance institutions adopt specialized climate risk assessment tools to project farm-level financial outcomes. Regulatory compliance is also evolving, with new frameworks requiring lenders to stress-test their agricultural portfolios against these automated climate volatility metrics.

The Strategic Action Plan: Preparing for Autonomous Farm Wallets

The convergence of artificial intelligence, decentralized finance, and agricultural hardware is creating a new operational paradigm. Agribusiness executives and institutional investors must adapt their technological infrastructure to support this shift.

Strategic Trajectory

- Operationalize Autonomous Farm Wallets to support rising Machine-to-Machine (M2M) payment requirements.

- Integrate decentralized finance (DeFi) protocols to enable autonomous tractors and drones to execute fuel and maintenance transactions.

- Deploy Regenerative Finance (ReFi) tools to automate the tokenization of carbon sequestration data.

- Establish infrastructure for real-time sustainable practice premium payments sourced directly from global ESG investors.

- Transition toward zero-intervention agricultural finance where maintenance transactions occur without human mediation.

The coming years will see the explosive rise of autonomous farm wallets. As agricultural hardware becomes fully autonomous, the financial transactions associated with that hardware must also become autonomous. We are entering the era of machine-to-machine payments.

In this near-future state, an autonomous tractor will monitor its own fuel levels and predictive maintenance needs. It will then interact with a decentralized finance protocol to autonomously pay for its own refueling or parts ordering, completely bypassing human intervention.

Simultaneously, we expect the massive emergence of regenerative finance tools. Global ESG investors are desperate for verifiable carbon credits. Farms are the ultimate carbon sinks, but the verification process has historically been too expensive.

ReFi tools solve this by automatically tokenizing carbon sequestration data pulled from soil sensors and satellite imagery. This allows farmers to receive real-time premium payments for sustainable practices directly from global institutional investors. It transforms regenerative farming from a moral choice into a highly lucrative financial strategy.

Conclusion: The Future of Smart Agricultural Money

The AgriFinTech ecosystem is no longer a niche sub-sector of financial technology. It is the vanguard of how global capital intersects with the physical world. By replacing manual underwriting with Decision Intelligence Finance, the industry has solved the historical problem of information asymmetry.

As we move toward a future defined by autonomous farm wallets, embedded procurement liquidity, and real-time parametric insurance, the definition of agricultural banking will fundamentally change. The winners in this space will be the institutions that stop viewing farms as biological risks, and start viewing them as data-rich financial nodes.

Navigating the intersection of financial technology, institutional capital, and market psychology requires a sharp strategy. To future-proof your FinTech architecture and scale with precision, connect with Andres at Andres SEO Expert.

Frequently Asked Questions

What is the projected market valuation for the AgriFinTech sector?

The global AgriFinTech market reached $7.29 billion in 2024 and is projected to grow to $64.69 billion by 2035. This expansion is fueled by the transition of agricultural operations into data-rich financial nodes that utilize unified orchestration layers.

How does technology eliminate information asymmetry in agricultural lending?

AgriFinTech tools utilize spectral satellite imagery and AI-driven analytics to monitor biological metrics like crop health and soil moisture. This transforms a farm’s biological data into verifiable financial metadata, allowing for collateral-free lending that bypasses the need for traditional physical land titles.

What is Decision Intelligence Finance in the context of agribusiness?

Decision Intelligence Finance refers to the integration of predictive analytics, real-time data feeds, and automated capital deployment. It enables instant liquidity by translating real-time farming operations into dynamic credit scores, which has reduced interest rates for data-rich farmers from historic highs of 60% down to approximately 12%.

How does parametric insurance disrupt traditional crop protection models?

Parametric insurance replaces manual loss adjustment with automated, data-triggered payouts. Using hyper-local weather data and satellite feeds, smart contracts execute payments instantly when specific environmental thresholds are breached, improving claim settlement speeds by 30% to 40%.

What are autonomous farm wallets and machine-to-machine (M2M) payments?

Autonomous farm wallets are financial tools integrated into autonomous agricultural hardware. They allow machinery, such as tractors or drones, to use decentralized finance (DeFi) protocols to independently execute and pay for refueling, parts, or maintenance without human mediation.

How do Regenerative Finance (ReFi) tools benefit sustainable farming?

ReFi tools automate the tokenization of carbon sequestration data using soil sensors and satellite imagery. This allows farmers to receive real-time premium payments for sustainable practices directly from global ESG investors, turning regenerative agriculture into a verifiable and lucrative financial strategy.