Key Points

- Agentic Finance Automation: AI agents now manage personal treasury operations, executing daily tax-loss harvesting and real-time portfolio rebalancing across multiple currencies.

- Elimination of the Liquidity Gap: Streamed Pay protocols utilizing FedNow and SEPA Instant rails have replaced the bi-weekly payroll cycle, instantly routing funds upon task verification.

- Predictive Consumption Models: Future AWFS iterations will autonomously pre-purchase essential services during market troughs, leveraging LLM forecasting to boost purchasing power by up to 15%.

Table of Contents

The Liquidity Gap Friction

According to a May 2026 report by the McKinsey Global Institute, the adoption of Streamed Pay protocols has reduced reliance on high-interest short-term credit by 58% among global gig workers compared to 2024 levels. This staggering shift signals the death of the traditional 30-day invoice cycle. The friction of the Liquidity Gap—that agonizing dead time between work performed and capital received—is finally being eradicated.

Enter the Autonomous Worker Financial Stack (AWFS). This is not just a digital wallet or an iterative neo-banking feature. It is a fundamental rewiring of how human capital interfaces with global liquidity.

The AWFS treats the individual worker as a micro-corporation equipped with a hyper-personalized algorithmic treasury. Smart money is shifting rapidly from generic consumer banking interfaces toward this highly specialized vertical labor fintech. By transforming the financial burden of self-employment into a frictionless background process, the AWFS unlocks unprecedented economic mobility.

Market Intelligence and Capital Flow

Market Intelligence & Data

Real-Time Payroll Volume

The total projected global transaction volume for real-time, task-based payments by the end of 2026, according to Juniper Research.

AI Agent Adoption

The percentage of ‘Power Users’ in the freelance economy who have delegated at least 80% of their financial administration to autonomous AI agents, per Deloitte’s 2026 Fintech Pulse.

Agentic Finance VC Flow

Total venture capital investment in startups specifically building ‘Individual Treasury’ tools in the first five months of 2026, as tracked by PitchBook.

The Yield Alpha

The average annual increase in net savings for workers using AI-optimized automated ‘Sweeps’ versus traditional banking, according to the 2026 Barron’s Wealth Tech Report.

This data paints a vivid picture of where institutional capital is currently flowing. Venture capital is no longer interested in funding superficial banking apps with colorful debit cards. Instead, over $1.2 billion has flooded into Agentic Wealth platforms like PayFlow AI and Nexus Individual in early 2026 alone.

These platforms automate the Personal CFO experience for the modern freelance economy. The massive projection for real-time payroll volume underscores a systemic shift in global infrastructure. We are witnessing the total convergence of payroll, tax-optimized investing, and real-time decentralized treasury management.

A recent McKinsey report on embedded finance and earned-wage access highlights how deeply integrated these payment layers are becoming within the broader labor economy. Institutional capital is racing to build the underlying rails that will support this automated, agent-driven financial future.

The Agentic Finance Deep Dive

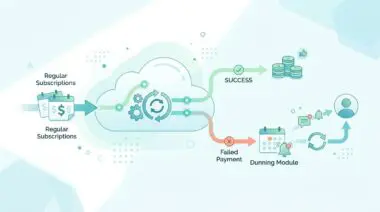

The 2026 worker stack is defined by what industry insiders call Agentic Finance. Autonomous AI agents now manage personal treasury operations in the background without any human intervention. Earnings flow instantly into programmable sub-accounts the exact moment a task is verified via smart contract or IoT-log.

AI-driven Tax-Loss Harvesting now occurs daily rather than annually. This relentless optimization maximizes net-take-home pay through hyper-personalized algorithmic management. The financial burden of self-employment transforms entirely into a frictionless, automated background process.

The Mechanics of Agentic Finance

At the core of the AWFS is a sophisticated routing engine powered by machine learning algorithms. These algorithms analyze real-time market conditions to determine the most capital-efficient destination for incoming funds. Whether sweeping excess cash into high-yield decentralized finance protocols or purchasing fractional shares of stable assets, the system operates with institutional-grade precision.

This is a radical departure from the passive asset holding models of the past decade. The individual worker’s treasury is now an active, dynamic entity capable of real-time market navigation. The AI agents continuously monitor liquidity needs, ensuring that enough capital is available for daily expenses while aggressively deploying the surplus to generate yield.

Streamed Pay and Decentralized Identity

Utilizing FedNow and SEPA Instant rails, Streamed Pay has completely replaced the archaic bi-weekly payroll cycle. This instantaneous transfer of value is authenticated through robust decentralized identity frameworks. The scale of this infrastructure is massive, aligning perfectly with a Juniper Research projection on global real-time payments that forecasts unprecedented transaction volumes.

Data from the 2026 Gartner Finance Symposium indicates that 22% of professional contractors now utilize Agentic Tax Escrows that automatically rebalance portfolios across three different currencies to hedge against inflation in real-time. This level of sophistication was previously reserved exclusively for institutional hedge funds. Today, it is a standard, out-of-the-box feature within the independent worker’s toolkit.

On-Chain Income Share Agreements

The AWFS also introduces decentralized protocols that allow workers to collateralize their future earnings on-chain. Through smart contract-enabled Income Share Agreements, workers can access upfront liquidity without relying on predatory lenders. This mechanism essentially allows the individual to issue personal equity based on verified historical earning data.

Investors can fund a worker’s upskilling or geographic relocation in exchange for a programmatic slice of future streamed pay. The blockchain ensures total transparency and automates the repayment process seamlessly. This innovation democratizes access to capital, treating human potential as a highly liquid, investable asset class.

The Global Labor OS Evolution

Legacy players like Brex and Revolut have recognized this paradigm shift and rapidly evolved into Global Labor OS providers. They are fiercely competing with decentralized protocols to capture the lucrative Global Nomad economy. By solving the friction of multi-jurisdictional tax compliance, these platforms ensure total portability of benefits for workers who frequently change geographic locations.

Regulatory frameworks are currently scrambling to catch up with these borderless financial primitives. However, automated compliance layers built directly into the AWFS ensure that cross-border tax liabilities are settled instantly via smart contracts. This keeps the worker fully compliant across multiple global jurisdictions without requiring any manual intervention or expensive accounting consultations.

The Strategic Action Plan

Strategic Trajectory

- Anticipate the 18-month transition to Biometric Treasury systems where agents execute micro-trades based on real-time productivity.

- Implement automated payment routing protocols that leverage verified health and performance data for liquidity optimization.

- Pivot toward Predictive Consumption models that autonomously secure essential services during market price troughs.

- Deploy LLM-driven market forecasting to systematically enhance the individual worker’s purchasing power by up to 15%.

- Transition from passive asset holding to an active, autonomous treasury stack capable of real-time market navigation.

Founders and institutional investors must pivot immediately to capture the immense value generated by this vertical labor fintech. Passive asset holding is entirely obsolete in an era where AI agents actively navigate real-time markets on behalf of the individual. Institutions should focus their capital on building or acquiring platforms that integrate seamlessly with these emerging autonomous systems.

The integration of LLM-driven market forecasting into personal finance apps is no longer a luxury; it is a baseline requirement. Companies that fail to offer predictive liquidity management will rapidly lose market share to platforms that actively increase a user’s purchasing power. The race is on to build the most intelligent, frictionless routing engine for human capital.

Preparing for the Biometric Treasury

The next 18 months will see the explosive rise of the Biometric Treasury. Financial agents will begin executing micro-trades and payment routing based on the worker’s real-time productivity metrics and verified health data. This convergence of wearable technology and decentralized finance represents the ultimate frontier of the AWFS.

By tying liquidity optimization directly to physical and cognitive output, the financial stack becomes a true extension of the worker’s biology. Executives must begin architecting API layers capable of ingesting secure biometric data to inform automated treasury decisions. Those who master this integration will define the next decade of consumer financial technology.

The Future of Predictive Consumption

We are moving rapidly toward an era of Predictive Consumption, where the worker’s stack doesn’t just hold money but autonomously pre-purchases essential services and commodities. By executing these purchases during market price troughs, the AI leverages LLM-driven forecasting to increase the worker’s purchasing power by up to 15%. This is the true promise of Agentic Wealth.

The Autonomous Worker Financial Stack (AWFS) is undeniably the ultimate operating system for the future of global labor. It bridges the massive gap between decentralized technological infrastructure and everyday financial stability. As streamed pay and AI agents become ubiquitous, the concept of a traditional bank account will seem as antiquated as the paper ledger.

Navigating the intersection of financial technology, institutional capital, and market psychology requires a sharp strategy. To future-proof your FinTech architecture and scale with precision, connect with Andres at Andres SEO Expert.

Frequently Asked Questions

What is the Autonomous Worker Financial Stack (AWFS)?

The Autonomous Worker Financial Stack (AWFS) is a specialized fintech infrastructure that treats individual workers as micro-corporations. It utilizes AI agents and algorithmic treasuries to automate payroll, tax optimization, and wealth management, replacing traditional consumer banking with a frictionless financial operating system.

How does Streamed Pay eliminate the liquidity gap for gig workers?

Streamed Pay utilizes real-time payment rails like FedNow and SEPA Instant to transfer earnings the moment tasks are completed. This eliminates the traditional 30-day invoice cycle, providing workers with immediate access to capital and reducing reliance on high-interest short-term credit by up to 58%.

What role do AI agents play in Agentic Finance?

In Agentic Finance, autonomous AI agents manage a worker’s personal treasury without human intervention. These agents execute daily tax-loss harvesting, route excess cash into high-yield protocols, and perform real-time currency rebalancing to hedge against inflation and maximize net-take-home pay.

What are on-chain Income Share Agreements (ISAs)?

On-chain Income Share Agreements allow workers to collateralize future earnings for upfront liquidity. By issuing personal equity via smart contracts, workers can fund upskilling or relocation without predatory loans, while investors receive a programmatic, transparent slice of future streamed pay.

What is a Biometric Treasury and how does it function?

A Biometric Treasury is a system where financial agents execute micro-trades and payment routing based on a worker’s real-time productivity and health data. By integrating wearable technology with DeFi, the financial stack optimizes liquidity according to the individual’s physical and cognitive output.

How does Predictive Consumption increase worker purchasing power?

Predictive Consumption leverages LLM-driven market forecasting to autonomously pre-purchase essential services and commodities during price troughs. By timing these purchases algorithmically, the system can increase an individual worker’s purchasing power by up to 15% compared to traditional spending models.