Key Points

- Elimination of Execution Drag: Autonomous Agentic Finance utilizes Large Action Models to autonomously execute real-time treasury management and dynamic tax-loss harvesting, removing human cognitive fatigue from wealth creation.

- The Rise of Invisible Finance: Institutional capital is heavily funding agentic middleware, shifting the industry from passive dashboards to proactive, self-driving money systems that require zero manual input.

- Predictive Wealth Orchestration: The future of FinTech relies on Sovereign AI Wealth IDs that anticipate life events and automatically recalibrate risk profiles 6 to 12 months in advance across decentralized and traditional protocols.

Table of Contents

The Friction of Manual Wealth Management

According to a 2026 report from TD Stories, 55% of consumers now utilize AI-powered tools to manage their personal finances. This marks a massive 5.5x increase in adoption compared to 2025 metrics. This rapid behavioral shift signals the death of passive banking interfaces.

We are entering an era where financial technology actively executes complex strategies on your behalf. The catalyst driving this unprecedented transformation is Autonomous Agentic Finance. This technology fundamentally rewires how personal and institutional capital operates in real-time.

It replaces static dashboards and manual spreadsheets with dynamic, self-executing financial employees. In this new landscape, the industry has shifted entirely from passive applications to active agents. The cutting edge is now defined by Large Action Models that utilize Open Banking 3.0 APIs.

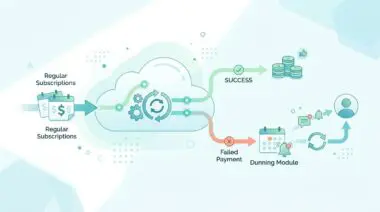

These systems move far beyond offering simple advice and step directly into autonomous execution. These intelligent agents seamlessly perform real-time treasury management and dynamic tax-loss harvesting. They also execute complex cross-chain yield optimization without requiring a single human click.

By integrating with real-time payment rails like FedNow and SEPA Instant, these systems completely eliminate settlement latency. The result is a financial ecosystem where personal capital achieves infinite velocity. Money moves between high-yield environments instantly, hunting for the best returns while you sleep.

This is the ultimate blueprint for leveraging advanced technology to achieve your financial goals faster.

Market Intelligence and the Flow of Smart Capital

To truly understand the magnitude of this shift, we must follow the institutional money. Venture capital and enterprise investments are flooding into the infrastructure that powers these self-driving money systems. The data paints a clear picture of a rapidly maturing market.

Market Intelligence & Data

Open Banking Penetration

Projections from CoinLaw indicate that over 33 million adults in the UK will be active open banking users by the end of 2026.

Tokenized Asset Volume

Research from Journeybee forecasts that tokenized Real-World Assets (RWAs) will surpass $500 billion in Total Value Locked by late 2026.

Agentic VC Influx

According to New Market Pitch, pure-play agentic AI financial startups raised $1.1 billion in equity funding in the first four months of 2026.

Robo-Advisory Share

Future Market Insights predicts that robo-advisors will command 30% of the AI-powered wealth management market by the conclusion of 2026.

The numbers above represent a fundamental restructuring of global financial infrastructure. When projections indicate that over 33 million adults will soon be active open banking users in the UK alone, the scale of adoption becomes undeniable. This level of penetration provides the necessary data layer for autonomous agents to function effectively.

Meanwhile, the explosion of tokenized Real-World Assets provides the programmable liquidity these agents require. As Total Value Locked surpasses half a trillion dollars, AI systems have a massive sandbox for yield generation. Capital is no longer siloed in legacy banking mainframes.

Furthermore, the massive influx of venture capital into pure-play agentic startups proves that institutional investors see the writing on the wall. They are funding the orchestration layers that will eventually replace traditional financial advisors entirely. The race to dominate invisible finance has officially begun.

The Infrastructure of Self-Driving Money

Overcoming the Execution Gap

The greatest hurdle to wealth creation is not a lack of information, but a lack of action. Autonomous finance directly solves what industry insiders call the execution gap. This is the widespread failure of consumers to act on profitable financial data due to sheer cognitive fatigue.

Modern consumers are overwhelmed by micro-decisions regarding their personal capital. They struggle to manually manage micro-investing, debt shuffling, and endless subscription cancellations. This friction results in approximately $2.5 trillion in trapped retail capital sitting idle in low-yield accounts.

Users simply lack the time, energy, or technical expertise to constantly reallocate their portfolios. Autonomous Agentic Finance eliminates this manual labor entirely. By automating thousands of micro-decisions, this technology effectively industrializes personal wealth creation.

The consumer appetite for this level of automation is already surging globally. A 2026 EY Global AI Sentiment Survey revealed that 49% of global consumers have actively used AI to support their savings and investment decisions within the last six months alone. People are ready to hand over the steering wheel to intelligent machines.

The Rise of Invisible Finance

Behind the scenes, institutional money is flowing heavily into agentic middleware. These are the agile startups providing the vital orchestration layer for AI financial employees. They are building the invisible pipes that connect disparate financial protocols into a single, cohesive brain.

Legacy incumbents like J.P. Morgan and Apple are aggressively integrating these financial operating system features into their consumer ecosystems. However, it is the disruptors like Flux and Sequoia-backed AutoCapital that are truly capturing the market. They are winning by offering completely invisible finance that requires zero manual input.

In this invisible paradigm, the user interface disappears entirely. Your financial agent works in the background, negotiating better loan rates and moving cash into higher-yielding protocols automatically. As Future Market Insights predicts, robo-advisors and their agentic successors will dominate the wealth management market shortly.

Naturally, this level of automation requires strict adherence to evolving data security frameworks. As these systems scale, they must operate within the strict boundaries of Open Banking 3.0 compliance and decentralized identity regulations. However, these regulatory guardrails are actually accelerating adoption by ensuring institutional-grade security for retail capital.

The Mechanics of Large Action Models

To grasp the power of autonomous finance, one must understand the underlying engine. Large Action Models represent a significant evolutionary leap over traditional language models. While language models generate text, action models generate verifiable financial transactions.

These models are trained on vast datasets of financial workflows, regulatory parameters, and market behaviors. They can read a smart contract, evaluate its risk parameters, and execute a token swap autonomously. This transforms artificial intelligence from a conversational novelty into a lethal financial weapon.

To fully leverage these systems, institutions must understand the three pillars of agentic architecture:

- Real-Time Treasury Management: The continuous, automated sweeping of idle cash into optimal yield-generating instruments.

- Dynamic Tax-Loss Harvesting: The algorithmic selling of underperforming assets to offset capital gains in real-time.

- Zero-Latency Settlement: The utilization of instant payment rails to eliminate the delay between trade execution and capital availability.

By leveraging Open Banking 3.0 APIs, these action models gain read-and-write access to traditional bank accounts. They can analyze your cash flow, determine your optimal liquidity buffer, and sweep excess funds into high-yield environments. All of this happens in milliseconds, completely bypassing the need for human approval.

Cross-Chain Yield Optimization

The true magic of agentic finance is realized when traditional banking merges with decentralized protocols. Cross-chain yield optimization allows AI agents to hunt for the highest possible returns across multiple blockchain networks. Capital is no longer restricted by geographic borders or legacy banking hours.

If a decentralized lending protocol on Ethereum offers a higher yield than a traditional savings account, the agent moves the funds instantly. It handles the complex bridging process, the currency conversion, and the smart contract execution. The user simply watches their net worth grow on a unified dashboard.

This level of sophistication was previously reserved for elite hedge funds and quantitative trading firms. Now, agentic middleware is democratizing this technology for the retail investor. It is the ultimate equalizer in the modern financial landscape.

The Strategic Action Plan for Predictive Wealth

For founders, executives, and institutional investors, the mandate is clear. Adapting to this agentic revolution requires a fundamental shift in how we build financial products. The next 12 to 24 months will separate the visionary platforms from the obsolete legacy applications.

Strategic Trajectory

- Transition to Predictive Wealth Orchestration to shift from reactive data management to proactive lifecycle anticipation.

- Utilize AI to forecast major medical expenses and education costs to preemptively recalibrate risk exposure.

- Automate liquidity adjustments 6-12 months in advance of projected life events to optimize capital efficiency.

- Adopt Sovereign AI Wealth IDs to establish portable, encrypted financial personas across institutional boundaries.

- Deploy lifelong financial proxies capable of acting across both traditional banking and decentralized protocols.

Implementing Predictive Wealth Orchestration

Moving from reactive dashboards to predictive wealth orchestration requires a massive overhaul of data architecture. Financial institutions must break down internal data silos to feed their AI models a holistic view of the customer. This includes integrating alternative data sources like healthcare projections and real estate market trends.

Once the data layer is unified, predictive algorithms can begin mapping out multi-decade financial trajectories. If the system anticipates a macroeconomic downturn, it can autonomously shift a user’s portfolio into defensive assets. This proactive recalibration preserves capital without requiring the user to panic-sell during a market crash.

Deploying Sovereign AI Wealth IDs

The concept of Sovereign AI Wealth IDs will fundamentally disrupt the traditional banking business model. Historically, banks relied on high switching costs to retain customers. In the agentic era, your financial identity becomes entirely portable and encrypted.

A Sovereign Wealth ID acts as your personal financial proxy, carrying your KYC data, risk profile, and investment history. You can plug this ID into any new financial institution or decentralized application instantly. The agent negotiates the terms of service, verifies the security protocols, and begins executing trades immediately.

This portability forces financial institutions to compete purely on yield and execution speed. If a bank offers subpar returns, the user’s agent will simply unplug and migrate their capital elsewhere. This hyper-competitive environment will drive unprecedented innovation across the entire FinTech sector.

The Future of Sovereign Capital

The era of manual wealth management is rapidly coming to a close. By deploying Autonomous Agentic Finance, individuals and institutions alike can achieve their financial goals faster than ever before. We are witnessing the birth of self-driving capital.

As these intelligent agents continue to evolve, they will unlock unprecedented levels of capital efficiency. The execution gap will vanish, and trapped retail liquidity will finally be unleashed into the broader economy. The smart money is already positioning itself for this autonomous future.

Navigating the intersection of financial technology, institutional capital, and market psychology requires a sharp strategy. To future-proof your FinTech architecture and scale with precision, connect with Andres at Andres SEO Expert.

Frequently Asked Questions

What is Autonomous Agentic Finance?

Autonomous Agentic Finance is an advanced technology that replaces manual wealth management with self-executing AI agents. These agents utilize Large Action Models and Open Banking 3.0 APIs to perform real-time treasury management, tax-loss harvesting, and yield optimization across financial protocols without requiring human intervention.

How do Large Action Models (LAMs) differ from traditional AI in finance?

While traditional language models focus on generating text, Large Action Models (LAMs) are designed to execute verifiable financial transactions. LAMs are trained on financial workflows and regulatory parameters, allowing them to read smart contracts, evaluate risk, and move capital autonomously.

What is the financial execution gap?

The execution gap refers to the failure of consumers to act on profitable financial data due to cognitive fatigue. This results in roughly $2.5 trillion in idle retail capital. Autonomous finance solves this by industrializing personal wealth creation and automating thousands of micro-decisions regarding debt, savings, and investments.

How does Open Banking 3.0 enable invisible finance?

Open Banking 3.0 provides the secure API infrastructure that allows AI agents to have read-and-write access to traditional bank accounts. This enables invisible finance, where agents operate in the background to negotiate better loan rates and sweep idle cash into high-yield instruments via real-time payment rails like FedNow.

What is a Sovereign AI Wealth ID?

A Sovereign AI Wealth ID is a portable, encrypted financial identity that contains a user’s KYC data, investment history, and risk profile. It allows users to instantly migrate their financial persona and capital between different institutions or decentralized protocols, forcing banks to compete purely on yield and execution speed.

How does cross-chain yield optimization work?

Cross-chain yield optimization involves AI agents searching for the highest possible returns across multiple blockchain networks and traditional banking systems. The agent handles the complex technical processes of bridging, currency conversion, and smart contract interaction to maximize a user’s net worth automatically.